Use an annealer or a genetic algorithm or other stochastic optimizer to solve the American put problem

Question:

Use an annealer or a genetic algorithm or other stochastic optimizer to solve the American put problem stated in the caption of Fig. 3.12. (A genetic algorithm is available at the web page for this text, www.math.gatech.edu/∼shenk; it is set up to use the pricing algorithm under the name amerputExerBoundary (for the reader to supply)).

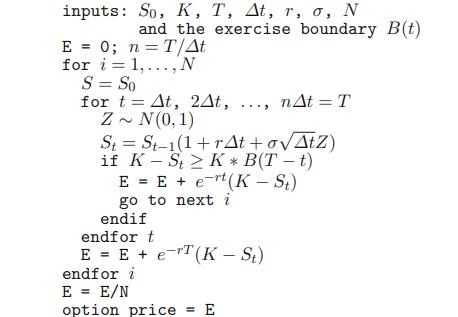

Data given in Algorithm 14

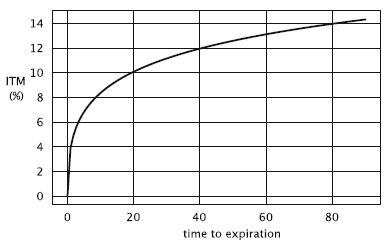

Figure 3.12

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Felix Onchweri

I have enough knowledge to handle different assignments and projects in the computing world. Besides, I can handle essays in different fields such as business and history. I can also handle both short and long research issues as per the requirements of the client. I believe in early delivery of orders so that the client has enough time to go through the work before submitting it. Am indeed the best option that any client that can think about.

5+ Reviews

19+ Question Solved

Related Book For

Question Posted: