Pet and Produce Ltd balances its books at monthend, uses special journals, and uses the perpetual inventory

Question:

Pet and Produce Ltd balances its books at month‐end, uses special journals, and uses the perpetual inventory system with the moving average cost flow assumption. All purchases and sales of inventory are made on credit. The end of the reporting period is 31 December. Ignore GST.

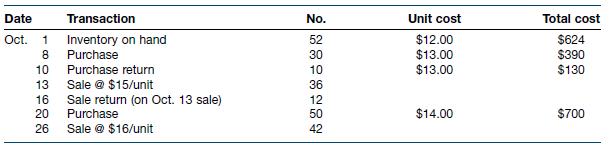

Sales and purchases of product AZL‐002 in October 2019 were as follows.

Accounts Receivable Control and Accounts Payable Control ledger account balances at 31 October 2019 were $86 600 Dr and $82 470 Cr respectively.

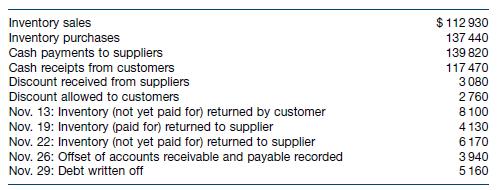

Transactions involving Pet and Produce Ltd’s customers and suppliers for November 2019 were as follows.

The Inventory Control ledger account balance at 31 December 2019 was $85 590, and net realisable value for each product line exceeded cost. The cost of inventory on hand at 31 December 2019 determined by physical count, however, was only $83 510. In investigating the reasons for the discrepancy, Pet and Produce Ltd discovered the following.

• Goods costing $1150 were ordered on 26 December 2019 on EXW terms. The transport firm took possession of the goods from the supplier on 28 December 2019. The purchase was recorded on 28 December 2019 but, as the goods had not yet arrived, the goods were not included in the physical count.

• $1860 of goods held on consignment for Druin Ltd were included in the physical count.

• Goods costing $980 were sold for $1130 on 29 December 2019 on DDP terms. The goods were in transit at 31 December 2019. The sale was recorded on 28 December 2019 and the goods were not included in the physical count.

Required

(a) For product AZL‐002, calculate October 2019’s cost of sales and the cost of inventory on hand at 31 October 2019. (Round each average unit cost to the nearest cent, but round each total cost amount to the nearest dollar.)

(b) Prepare the Accounts Receivable Control and Accounts Payable Control general ledger accounts (T‐format) for the period 31 October to 30 November 2019.

(c) Prepare any journal entries necessary on 31 December 2019 to correct error(s) and adjust inventory. (Use the general journal.)

Step by Step Answer:

Financial Accounting

ISBN: 9780730363217

10th Edition

Authors: John Hoggett, John Medlin, Keryn Chalmers, Claire Beattie, Andreas Hellmann, Jodie Maxfield