Ocado Group plc: reporting inventory Ocado- How? Established in 2000 and listed on the London Stock Exchange

Question:

Ocado Group plc: reporting inventory Ocado- How?

Established in 2000 and listed on the London Stock Exchange in July 2010, Ocado is the world’s largest dedicated online grocery retailer, with over 580,000 active customers. Our objective is to provide our retail and corporate customers with the best proposition in online shopping at the lowest possible operating cost.

This enables us to build a strong, sustainable and growing business designed to deliver long-term value for our shareholders.

Strategic report

We face the unique challenge that around half of our sales lie within fresh and chilled categories and as a delivery operation we have to ensure this freshness is preserved right up to our customers’ front doors. To enable this we operate a shelf life promise whereby a minimum of approximately two-thirds of the total life of the product is guaranteed by the time it reaches the customer. In traditional store-based competitors this is difficult for a number of reasons including additional human touchpoints and disrupted stock rotation due to manual customer intervention as they personally handle the products.

Our model enables us to carry lower inventory levels and to operate a perfect “first in first out” stock rotation dependent on shelf life. This allows us to operate with what we believe to be the lowest product waste in the industry at 0.7% of sales across our CFCs and underlines the sustainability benefits of our operating model.

Accounting policy: inventories

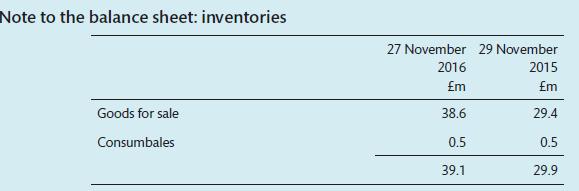

Inventories comprise goods held for resale, fuel and other consumable goods. Inventories are valued at the lower of cost and net realisable value as provided in IAS 2 “Inventories”. Goods held for resale and consumables are valued using the weighted average cost basis. Net realisable value represents the estimated selling price less all estimated costs of completion and costs to be incurred in marketing, selling and distribution. It also takes into account slow-moving, obsolete and defective inventory. Fuel stocks are valued at calculated average cost. Costs include all direct expenditure and other appropriate attributable costs incurred in bringing inventories to their present location and condition. There has been no security granted over inventory unless stated otherwise.

The Group has a mix of grocery and general merchandise items within inventory which have different characteristics. For example, grocery lines have high inventory turnover, while non-food lines are typically held within inventory for a longer period of time and so run a higher risk of obsolescence. As inventories are carried at the lower of cost and net realisable value, this requires the estimation of the eventual sales price of goods to customers in the future. Judgement is applied when estimating the impact on the carrying value of inventories such as slow-moving, obsolete and defective inventory, which includes reviewing the quantity, age and condition of inventories throughout the year.

Discussion points

1 What do you discover about the valuation of inventory from the strategic report?

2 What do you discover about the valuation of inventory from the accounting policy?

3 How do the narrative descriptions provide deeper understanding of the figures in the balance sheet for inventory?

Step by Step Answer:

1 The strategic report helps understand the amount of inventory and the attentio...View the full answer