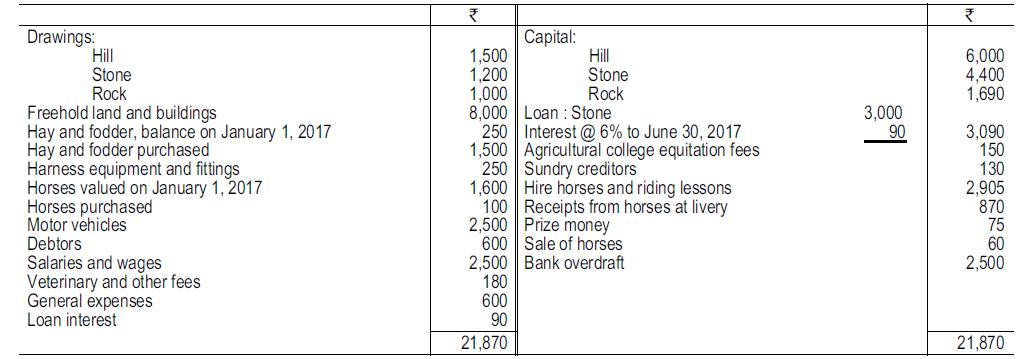

Hill, Stone and Rock were in partnership owning a riding school and livery stables. Profits and losses

Question:

Hill, Stone and Rock were in partnership owning a riding school and livery stables. Profits and losses were shared : Hill three- fifths, Stone one-fifth, Rock one-fifth. No interest was charged on drawings or credited on capital. The firm provided an instructor to the equitation classes of the local agricultural college. The following was a summary of the Balances as on 31 December, 2017. On 31 December 2017, hay and fodder were valued at ₹50, motor vehicles at ₹2,000, harness, equipment and fittings at ₹200, and horses at ~ 1,400. Provision was needed for veterinary fees ₹50. With the exception of loan interest no further provisions were considered necessary.

On 31 December 2017, hay and fodder were valued at ₹50, motor vehicles at ₹2,000, harness, equipment and fittings at ₹200, and horses at ~ 1,400. Provision was needed for veterinary fees ₹50. With the exception of loan interest no further provisions were considered necessary.

The partnership was dissolved on 31 December 2017, on the following terms :

1. Rock was appointed instructor to the local agricultural college, and for this privilege, he paid into the partnership ₹200 which is to be divided between Hills and Stone.

2. He also took over assets at the following valuation:

(i) six horses ₹600;

(ii) the hay and fodder ₹40;

(iii) part of the harness and equipment ₹75;

(iv) a horse box ₹800.

3. Hill took over a motor car at a valuation of ₹450.

4. Net receipts from the sale of the freehold and buildings amounted to ₹8,750.

5. The debtors realised ₹530 and the remaining assets were sold by auction, the net receipts being ₹1,765.

6. The loan, with interest accrued to date, was repaid on 1 January, 2018.

7. The creditors were paid and a contingent liability, not brought into the accounts, was settled early in January for ₹250.

8. Cups and plate, not brought into the accounts, were distributed among the partners at the following valuation :

Hill ₹20, Stone ₹10, Rock ₹60. All transactions were completed and all amounts receivable or payable by the partners were settled before the end of January 2018.

You are required to prepare :

(a) The Profit and Loss Account for the year ended 31 December 2017, excluding any profits or losses arising on dissolution; (b) The Realisation Account; (c) The Cash Account; and (d) Partners’ Capital Accounts showing the final settlement on dissolution.

Step by Step Answer:

1 Prepare the Profit and Loss Account for the year ended December 31 2017 excluding dissolution profits or losses Particulars Amount Incomes Agricultu...View the full answer

Financial Accounting Volume II

ISBN: 9789387886230

4th Edition

Authors: Mohamed Hanif, Amitabha Mukherjee