Risk directly affects the values of professional teams. Groppelli and Nikbakht (2012) state that to maximize the

Question:

Risk directly affects the values of professional teams. Groppelli and Nikbakht (2012) state that to maximize the value of a firm, managers must focus on increasing the growth rate of cash flows and reducing the risk or uncertainty of those cash flows. One measure of an organization’s risk is its credit rating. According to Fitch Ratings (2002), factors affecting the risk of cash flows and, therefore, the credit rating of leagues and teams, include player salary restraints, national television contracts, revenue sharing among member clubs, league influence on team financial matters, debt limits, and the relationship with the players’ union. Exhibit 3.11 compares the average franchise value for the NFL and MLB from 2010 through 2014. The fact that the average value of an NFL franchise is more than 75% greater than that of the average MLB franchise in 2014 is due in part to differing levels of risk. Fitch Ratings discussed the factors that led to its conclusion that the NFL has the highest credit rating of all leagues. Primarily, the NFL is best able to withstand economic slowdowns that affect sponsorships, naming rights agreements, and the disposable income of fans. Its risk is reduced by lucrative long-term contracts with its media partners, strong relations with the NFL Players Association (NFLPA), and the willingness of team owners to be proactive in working together for the betterment of the league. The teams cooperate on merchandising and licensing revenues and have agreed to the creation of a leaguefunded loan pool to help individual franchises build new stadiums that will increase local revenues. Further, the league is the most competitively balanced from top to bottom, thanks to its hard salary cap. The hard cap controls the largest team expense, reducing the risk of team financial losses and improving the league’s creditworthiness. The NFL also limits the debt that a franchise can incur, reducing risk for both the league and its teams. Fitch Ratings rates the creditworthiness of MLB lower than that of the NFL because the MLB is exposed to greater risk. Although revenue sharing has increased under the latest MLB CBA, teams share only a small percentage of overall television revenue. Each team is able to negotiate and keep most (or, for some teams, all) of its local television revenues. The league does not have a hard salary cap, and although labor relations have improved greatly, MLB and the players association have a history of poor relations. Fitch Ratings notes that as MLB moves its economic model closer to that of the NFL, its risk will decrease and its rating will improve. This can be seen in the narrowing gap between franchise values of the NFL and MLB from 2011 to 2013. During that time frame, MLB values increased at a greater rate than NFL values, as MLB had secured more money from its television rights deals and increased the value of Major League Baseball Advanced Media (MLBAM) and the revenues derived from MLBAM.

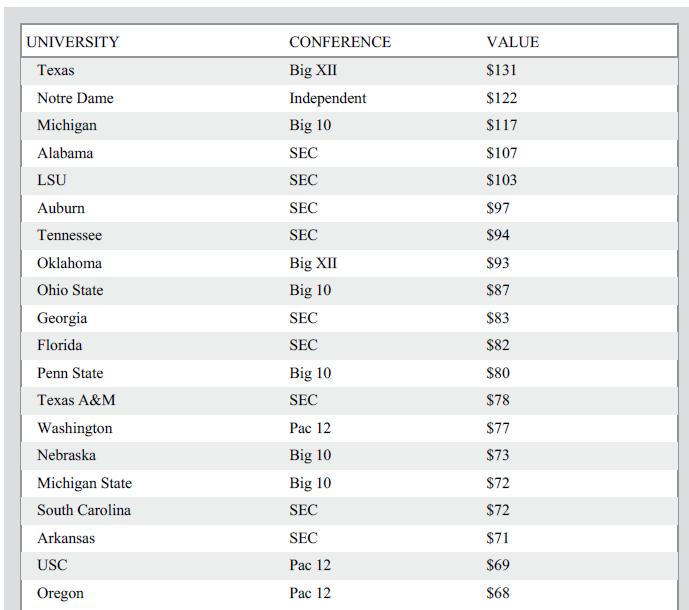

MLB’s television rights deals with Fox, TBS, and ESPN are now worth more than twice what the league was receiving under its previous rights deals (Ozanian, 2013). However, after the NFL’s new broadcasting deals with NBC, ESPN, CBS, and Fox began in 2014, revenues received by each team from media rights increased \($80\) million per year (Ozanian, 2014). This new revenue resulted in NFL team values growing 22% in 2014, while MLB values grew 9%. The importance of acquiring and securing revenue sources and the impact of doing so on risk and value is evident in an examination of collegiate football teams (see Exhibit 3.12). Forbes calculates the value of NCAA Division I – FBS teams in its reporting on the revenues of athletic programs. Exhibit 3.12 lists the 20 most valuable football teams in 2014. The average value of these teams was \($88.8\) million. The list clearly indicates that teams in conferences with higher cash flows and lower risk or uncertainty of those cash flows are more highly valued than teams in conferences without lucrative longterm media contracts. (In Notre Dame’s case, the team itself has secured these contracts.) For example, the SEC has nine of the 20 most valuable teams, according to Forbes. The league has a lucrative contract to broadcast football games nationally, and revenue from that contract flows back to its member schools. Further, the league launched the SEC Network in partnership with ESPN in August 2014. Notre Dame’s contract with NBC provides similar revenues. The Big 10, with five teams listed, created its own television network to generate revenues for member institutions. A recent history of winning has little impact on a team’s value. Texas has struggled for several years but is ranked as the most valuable program. Florida has struggled since Urban Meyer left, but the team benefits from its membership in the SEC. The value of the Florida football team is \($5\) million greater than that of the University of Washington team—which is the highest-valued Pac 12 team.

EXHIBIT 3.11 Average value (in millions) of NFL and MLB franchises from 2010 to 2014.

Exhibit 3.12 Valuations of college football teams in 2014 (millions).

case questions

1. What current economic conditions might affect the credit rating of a team or league?

2. Which teams’ credit ratings might be most negatively affected during a recession?

3. What must the NFL do to maintain its high credit rating?

4. What can MLB do to improve its credit rating?

Step by Step Answer: