Question: Consider the two GBMs which are driven by the same standard Wiener process. - Find the stochastic differential equation for the process - Imagine

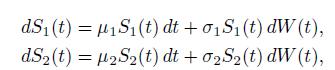

Consider the two GBMs

which are driven by the same standard Wiener process.

- Find the stochastic differential equation for the process

- Imagine a Finnish investor, whose home currency is EUR, investing on the US stock market. The stock price in EUR is the product of the stock price in USD and the exchange rate between the two currencies. Would you use the above model in this case? Why or why not?

dS1(t)=1S1(t) dt + S (t) dW (t), dS2(t)=2S2(t) dt + 2S2(t) dW (t),

Step by Step Solution

★★★★★

3.26 Rating (144 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock