A hedge fund specializes in investments in emerging market sovereign debt. The fund manager believes that the

Question:

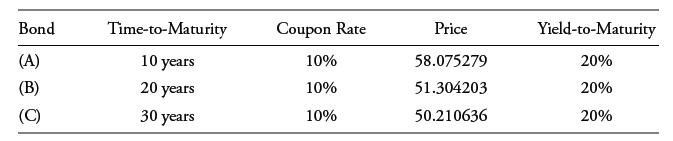

A hedge fund specializes in investments in emerging market sovereign debt. The fund manager believes that the implied default probabilities are too high, which means that the bonds are viewed as “cheap” and the credit spreads are too high. The hedge fund plans to take a position on one of these available bonds.

The coupon payments are annual. The yields-to-maturity are effective annual rates. The prices are per 100 of par value.

Which of the three bonds is expected to have the highest percentage price increase if the yield-to-maturity on each decreases by the same amount—for instance, by 10 bps from 20% to 19.90%?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Despite the significant differences in timestomaturity 10 20 and 30 years the a...View the full answer

Answered By

David Ngaruiya

i am a smart worker who concentrates on the content according to my clients' specifications and requirements.

7+ Reviews

19+ Question Solved

Related Book For

Question Posted: