An investor observes the following current CDS market information: Select the most appropriate credit portfolio positioning strategy

Question:

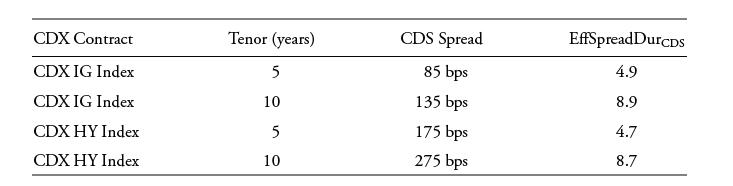

An investor observes the following current CDS market information:

Select the most appropriate credit portfolio positioning strategy to capitalize on an expected steepening of the investment-grade credit spread curve.

A. Sell protection on the 10-year CDX IG index and purchase protection on the 5-year CDX IG index using contracts of equal notional value.

B. Sell protection on the 10-year CDX IG index and purchase protection on the 5-year CDX IG index using a contract with a notional amount equal to 1.82 times that of the 10-year contract.

C. Buy protection on the 10-year CDX IG index and sell protection on the 5-year CDX IG index using a contract with a notional amount equal to 1.82 times that of the 10- year contract.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

RADHIKA MEENAKAR

I am a qualified indian Company Secretary along with Masters in finance with over 6 plus years of professional experience. Apart from this i am a certified accounts and finance tutor on many online platforms.

My Linkedin profile link is here https://www.linkedin.com/in/radhika-meenakar-88b9808a/

12+ Reviews

22+ Question Solved

Related Book For

Question Posted: