It was 5:30 Friday afternoon, January 22, 2016. Bill Hall, the chairman and CEO of National Brands

Question:

The phone rang. It was Maria Ortiz, his secretary. "Did you hear the latest on the news wire?" Maria asked.

"No, what's up?" Bill replied, with a suspicious feeling that his evening wasn't going to be so relaxing after all.

"Kelly O'Brien, head of A-1 Holdings, just announced that he's bought 5 percent of our outstanding shares, and now he's making a tender offer for all of the rest at $55."

"I knew it!" Bill spat out. "He was in here just a few weeks ago, talking about whether we would sell the company to him. We turned down his offer because we want to stay independent, and he left after implying that we weren't looking out for our shareholders.

He's got some plan to restructure the company around a six-member board of directors instead of the 15 we have now. Now he's trying to do it anyway, whether we like it or not!"

"Looks like it," Maria agreed. "So what do you think we should do?" "OK, contact Tom Straw, the chief operating officer and Doris Faraday in finance, and tell them to get up here for a meeting right away," Bill directed. "Oh, and have Stan Lindner from public relations come, too; we're sure to have a press release about this, and-oh, wait-call my wife and tell her I won't be home until late tonight."

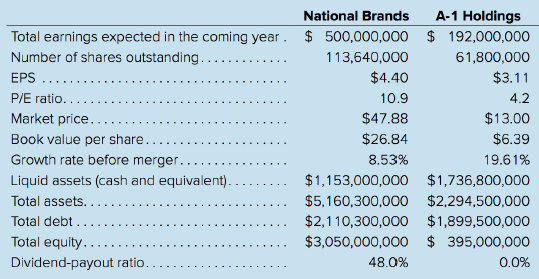

After about half an hour, those that Bill had called for began arriving, armed with pencils, papers, and calculators in anticipation of the coming session. Bill, in the meantime, had managed to compile some financial data about A-1 Holdings, which he had summarized on a sheet of paper along with like data about his own company, National Brands, for comparison (see Table 1) . He passed the sheet around among the others.

"OK, let's start with what we know," Bill led off. "A-1 already has 5 percent of our outstanding shares, and it is making a bid for the rest at $55, or 7.875 over market."

"I hate to be the devil's advocate," Stan said, thinking of the 25,000 shares he owned personally, "but that sounds like a pretty fair offer. What will happen if he succeeds?"

"Most of us will be out of a job, and this company will become just another card in Kelly O'Brien's poker hand," Bill said acidly. "Our employees deserve better than that, so let's talk about what we can do to keep it from happening."

"What about a poison pill?" Tom suggested. "We could take out a fair-sized loan based on our heavy cash position, and A-1 would have a tough time absorbing it-just look at the amount of debt they're carrying now!"

"That would probably work, but it's not very good for us, either," Stan agreed. He was still thinking about the $7 a share profit to be made in a buyout. "So how about someone else? You know, a white knight that would top A-1's offer but would keep the structure of the company substantially the same as it is now."

"I don't know who we could ask," Bill said, "and besides that, the basic problem would probably still occur-we would lose our status as an independent entity."

Doris had been working on some figures on her pad, and she spoke up now. "There's another alternative," she said, "that I'm surprised you all haven't mentioned, given the financial status of the two companies."

"What, what!" Bill said. "Don't keep us in suspense!"

"It's the Pacman defence," she continued, unruffled. "What we do is launch a tender offer of our own for all of A-1's outstanding stock. If it's successful, we not only thwart the takeover attempt but we gain a new business in the bargain."

"Didn't Martin Marietta try that with Bendix back in 1989?" Bill asked. "As I recall, it didn't turn out very well for them."

"You're right; it didn't," Doris agreed, "and no one else has tried it since. But just comparing the numbers here between National and A-1 , I think it might work out quite well for us. I've been doing some calculating here, and I think an offer to A-1's shareholders of $17 a share would be accepted, and we could conclude the whole affair rather quickly."

Table 1

"I'm interested." Bill said. "Tell you what: Put your finance staff on it over the weekend and have them work up the proposal formally. Get the legal and accounting people to help you too. In the meantime, Stan, tip off the news media that we will have an announcement of our own shortly and draft up a public notice for A-1's shares at $17 each. Don't release it yet, but be ready to on Monday. Oh, and be sure to include in it that I said the deal will not cause any dilution of National's EPS. One last thing; Doris, draft an open letter to our shareholders for my signature, explaining what's happening and reassuring them that we will keep their company intact and prosperous."

"Any questions? If not, let's get on it. Mr. O'Brien is about to get a surprise!"

a. (1) A-1 is offering $55 a share for National's stock. How much total cash will it have to raise to buy the company? (The remaining 95%?)

(2) Assume A-1 plans to borrow the money needed to make the purchase. If A-1 uses the amount of liquid assets presently on hand at National to offset the amount it needs to borrow, what is the net amount it will have to borrow?

(3) Assuming A-1 does borrow the amount you determined in (2) above, what will A-1 's total debt be after the purchase is completed? In making your calculation, consider all forms of debt that the combined firm will have. Now compute A-1's debt-to-equity ratio (A-1's equity will not increase) . Given this ratio , do you think it is likely that A-1 will be able to obtain the necessary debt financing?

(4) Suppose instead that A-1 decides to issue stock to raise the money needed for the purchase (i.e. , the amount you computed in (2) above will be raised through a stock issue instead of by borrowing). How many shares of A -1 stock will have to be issued? (Assume the price at which it will be issued is $13 and disregard flotation costs.)

(5) If A-1 raises the money by issuing new shares of its stock, what will A-1's EPS be after the purchase is complete and the earnings are combined?

(6) Do you think A-1's shareholders will be happy if this deal goes through? What about the current National shareholders?

b. (1) If National employs the Pacman defence and tries to buy A-1 for $17 a share, how much will the total dollar price be?

(2) If National wants to finance the purchase by issuing stock, and it plans to use the amount of liquid assets on hand at A-1 to offset the amount of stock that needs to be issued, what will the total dollar price be? (Assume they will be issued at $47.88 and disregard flotation costs.)

(3) What will be National's debt-to-equity ratio after the purchase is complete? (Assume it was completed per your calculations in part b (2) above.) That National's total equity will not increase since no new shares are issued.

(4) Suppose, instead, that National decides to first use A-1's liquid assets to pay down most of A-1's debt. How many shares of National at $47.88 will have to be issued? Use the cost figure from your answer to part b (1).

(5) What will the new National's EPS be, assuming the deal is completed per your calculations in part b (4) above?

(6) Is Bill Hall correct in his statement that National's EPS will not be diluted as a result of the purchase of A-1?

c. If National's P/E does not change following the purchase of A-1 , what will its stock price be? Is it likely that National's P/E will remain at 10.9? Or do you think it will rise or fall?

d. (1) Do you think National's Pacman defence will be successful? Or do you think A-1 will succeed in buying out National?

(2) Do you think that National's shareholders are better off as a result of A-1's attack and National's Pacman defence (assuming it succeeds)?

(3) Do you think Kelly O'Brien, head of A-1 , should be viewed as a "good guy," whose action will produce more efficient companies, or a "bad guy," who is a destroyer of traditional values and employees' careers?

Step by Step Answer:

This case features a surprise attack tender offer The acquisition candidate decides to counter with a Pac Man defense in which they make an offer for the potential acquiring company Both firms are con...View the full answer

Ethical Obligations And Decision Making In Accounting Text And Cases

ISBN: 9780078025280

2nd Edition

Authors: Steven Mintz, Roselyn Morris