Question: Problem 8 is the same as problem 7 with respect to initial measurement of the ARO liability. Now assume that Tadpoles credit standing improves over

Problem 8 is the same as problem 7 with respect to initial measurement of the ARO liability. Now assume that Tadpole’s credit standing improves over time, causing the credit-adjusted risk-free rate to decrease by 1% to 9% at December 31, 2019.

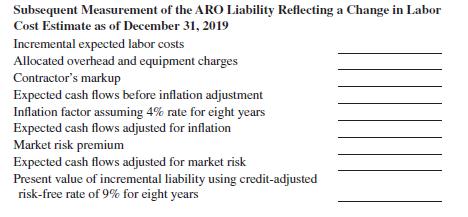

On December 31, 2019, Tadpole revises its estimate of labor costs and revised the probability assessments related to those labor costs. The change in labor costs results in an upward revision to the undiscounted cash flows. Consequently, the incremental cash flows are discounted at the current rate of 9%. All other assumptions remain unchanged. The revised estimate of expected cash flows for labor costs is as follows:

REQUIRED:

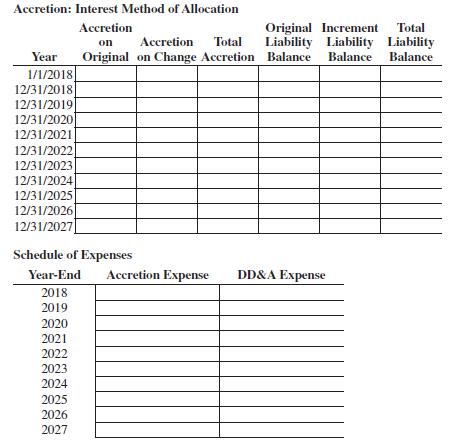

a. Complete the following tables:

b. Prepare the journal entry that would be made on January 1, 2018, to record the asset retirement obligation.

c. Prepare the journal entries that would be made on December 31, 2018, and December 31, 2019, to record the accretion expense and the DD&A expense related to the ARO.

d. Prepare the journal entries that would be required at December 31, 2019, to record the revision in the asset retirement obligation.

e. Prepare the journal entries that would be made from December 31, 2020, to December 31, 2027, to record the accretion expense and the DD&A expense.

f. On December 31, 2027, Tadpole settles its asset retirement obligation by using an outside contractor. It incurs costs of $800,000. Prepare the journal entries that would be made on December 31, 2027, to record the settlement of the asset retirement obligation.

Data From Problem 7:-

Tadpole Oil and Gas Company completes construction of an offshore oil platform and places it into service on January 1, 2018. Tadpole is legally required to dismantle and remove the platform at the end of its useful life, which is estimated to be 10 years. On January 1, 2018, Tadpole recognized a liability for an asset retirement obligation and capitalized an amount for an asset retirement cost. It estimated the initial fair value of the liability using an expected present value technique. The significant assumptions used in that estimate of fair value are as follows:

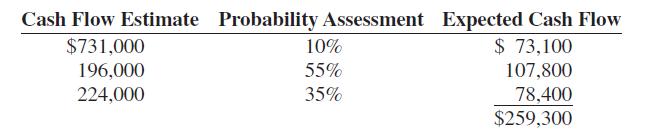

a. Labor costs are based on current marketplace wages required to hire contractors to dismantle and remove offshore oil platforms. Tadpole assigns probability assessments to a range of cash flow estimates as follows:

b. Tadpole estimates allocated overhead and equipment charges using the rate it applies to labor costs for transfer pricing (60%). The entity has no reason to believe that its overhead and equipment rate differs from that used by contractors in the industry.

c. A contractor typically adds a markup on labor, allocated internal costs, and equipment to provide a profit margin on the job. The entity determines the profit that contractors in the industry generally earn to dismantle and remove offshore oil platforms is 15%.

d. A contractor would typically demand and receive a premium (market risk premium) for bearing the uncertainty and unforeseeable circumstances inherent in “locking in” today’s price for a project that will not occur for 10 years. The entity estimates the amount of that premium to be 5% of the estimated inflation-adjusted cash flows.

e. The risk-free rate of interest on January 1, 2015 is 6%. The entity adjusts that rate by 4% to reflect the effect of its credit standing. Therefore, the credit-adjusted risk-free rate used to compute expected present value is 10%.

(Round the present value factor to four decimal places.)

f. Tadpole assumes a rate of inflation of 4% over the 10-year period. (Round the factor to four decimal places.)

Cash Flow Estimate Probability Assessment Expected Cash Flow $731,000 196,000 224,000 10% 55% 35% $ 73,100 107,800 78,400 $259,300

Step by Step Solution

3.52 Rating (152 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts