According to the pure expectations theory of interest rates, how much do you expect to pay for

Question:

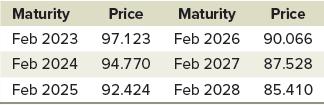

According to the pure expectations theory of interest rates, how much do you expect to pay for a one-year STRIPS on February 15, 2023? What is the corresponding implied forward rate? How does your answer compare to the current yield on a one-year STRIPS? What does this tell you about the relationship between implied forward rates, the shape of the zero coupon yield curve, and market expectations about future spot interest rates?

U.S. Treasury STRIPS, close of business February 15, 2022:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

1 02704 2 4 1 02941 2 2 1 11 11 02483 or 2483 EAR P 1 100 102483 9757...View the full answer

Answered By

OTIENO OBADO

I have a vast experience in teaching, mentoring and tutoring. I handle student concerns diligently and my academic background is undeniably aesthetic

3+ Reviews

10+ Question Solved

Related Book For

Fundamentals Of Investments Valuation And Management

ISBN: 9781266824012

10th Edition

Authors: Bradford Jordan, Thomas Miller, Steve Dolvin

Question Posted: