Vang Magazine Company started construction of a warehouse building for its own use at an estimated cost

Question:

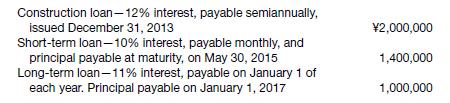

Vang Magazine Company started construction of a warehouse building for its own use at an estimated cost of ¥5,000,000 on January 1, 2014, and completed the building on December 31, 2014 (all amounts in thousands). During the construction period, Vang has the following debt obligations outstanding.

Total cost amounted to ¥5,200,000, and the weighted-average accumulated expenditures was ¥3,500,000.

Jane Edo, the president of the company, has been shown the costs associated with this construction project and capitalized on the statement of financial position. She is bothered by the “avoidable interest”

included in the cost. She argues that, first, all the interest is unavoidable—no one lends money without expecting to be compensated for it. Second, why can’t the company use all the interest on all the loans when computing this avoidable interest? Finally, why can’t her company capitalize all the annual interest that accrued over the period of construction?

Instructions You are the manager of accounting for the company. In a memo dated January 15, 2016, explain what avoidable interest is, how you computed it (being especially careful to explain why you used the interest rates that you did), and why the company cannot capitalize all its interest for the year. Attach a schedule supporting any computations that you use.

Step by Step Answer:

Intermediate Accounting IFRS Edition

ISBN: 9781118443965

2nd Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield