Question: Klerk Company had four temporary differences between its pretax financial income and its taxable income during 2019 as follows: At the beginning of 2019, Klerk

Klerk Company had four temporary differences between its pretax financial income and its taxable income during 2019 as follows:

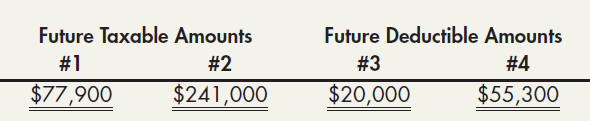

At the beginning of 2019, Klerk had a deferred tax liability of $84,300 related to Temporary Difference #2 and a deferred tax asset of $21,090 related to Temporary Difference #4. Based on its tax records, Klerk earned taxable income of $270,000 for 2019. Kerk’s accountant has prepared the following schedule showing the total future taxable and deductible amounts at the end of 2019 for its four temporary differences:

The company has a history of earning income and expects to be profitable in the future. The income tax rate for 2019 is 40%, but in 2018 Congress enacted a 30% tax rate for 2020 and future years. During 2019, for financial accounting purposes, Klerk reported revenues of $750,000 and expenses of $447,100. The deferred taxes related to Temporary Differences #1, #2, and #4 are considered to be noncurrent by the company; the deferred tax related to Temporary Difference #3 is considered to be current.

Required:

1. Prepare Klerk’s income tax journal entry for 2019.

2. Prepare a condensed 2019 income statement for Klerk.

3. Show how the income tax items are reported on Klerk’s December 31, 2019, balance sheet.

Number Temporary Difference Gross profit on certain sales is recognized under the accrual method for financial reporting and under the cash-basis method for income taxes. MACRS depreciation is used for income taxes; a different depreciation method is used for financial reporting. Rent receipts are included in taxable income when collected in advance; rent revenue is recognized under the accrual method for financial reporting. Warranty expense is estimated for financial reporting; warranty costs are deducted as incurred for income taxes. 4 Future Taxable Amounts #1 Future Deductible Amounts #2 #3 #4 $77,900 $241,000 $20,000 $55,300

Step by Step Solution

3.39 Rating (158 Votes )

There are 3 Steps involved in it

1 2019 Dec 31Income Tax Expense 117870 a Deferred Tax Asset 3 6000 b Deferred Tax Liability 2 12000 ... View full answer

Get step-by-step solutions from verified subject matter experts