Jacobsen Corporation is negotiating a loan for expansion purposes. Jacobsens books and records have never been audited

Question:

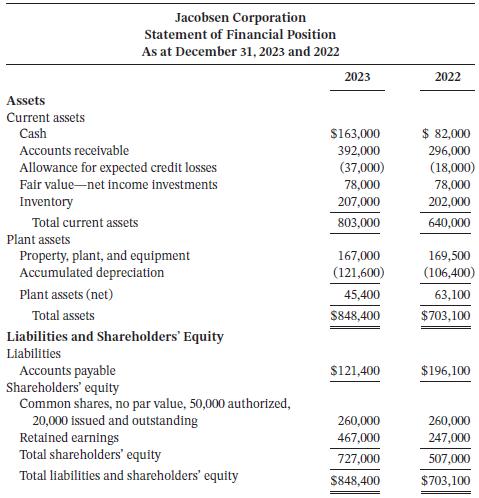

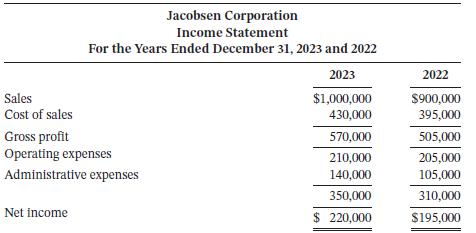

Jacobsen Corporation is negotiating a loan for expansion purposes. Jacobsen’s books and records have never been audited and the bank has requested that an audit be performed and that IFRS be followed. Jacobsen has prepared the following comparative financial statements for the years ended December 31, 2023 and 2022.

During the audit, the following additional facts were determined:

1. An analysis of collections and losses on accounts receivable during the past two years indicates a drop in anticipated credit losses. Management has decided that the loss experience rate on sales should be reduced from the recorded 2% to 1.5%, beginning with the year ended December 31, 2023.

2. An analysis of the FV-NI investments revealed that the total fair value for these investments as at the end of each year was as follows:

Dec. 31, 2022 $78,000Dec. 31, 2023 65,000

3. Inventory at December 31, 2022, was overstated by $8,900 and inventory at December 31, 2023, was overstated by $13,600.

4. On January 2, 2022, equipment costing $30,000 (estimated useful life of 10 years and residual value of $5,000) was incorrectly charged to operating expenses. Jacobsen records depreciation on the straight-line basis. In 2023, fully depreciated equipment (with no residual value) that originally cost $17,500 was sold as scrap for $2,800. Jacobsen credited the $2,800 in proceeds to the Equipment account.

5. An analysis of 2022 operating expenses revealed that Jacobsen charged to expense a four-year insurance premium of $4,700 on January 1, 2022.

6. The analysis also revealed that operating expenses were incorrectly classified as part of administrative expenses in the amount of $15,000 in 2022 and $35,000 in 2023.

Instructions

a. Prepare the journal entries to correct the books at December 31, 2023. The books for 2023 have not been closed. Ignore income tax effects.

b. Beginning with reported net income, prepare a schedule showing the calculation of corrected net income for the years ended December 31, 2023 and 2022, assuming that any adjustments are to be reported on comparative statements for the two years. Ignore income tax effects. (Do not prepare financial statements.)

c. Prepare a schedule showing the calculation of corrected retained earnings at January 1, 2023.

Step by Step Answer:

a b c 1 2 3 4 5 JACOBSEN CORPORATION Adjusting Journal Entries December 31 2023 Allowance for Expect...View the full answer

Intermediate Accounting Volume 2

ISBN: 9781119740445

13th Canadian Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Irene M. Wiecek, Bruce J. McConomy