Erskine Consulting Ltd. has been in business for several years, providing software consulting to its customers on

Question:

Erskine Consulting Ltd. has been in business for several years, providing software consulting to its customers on an annual contract or special assignment basis. All work is done over the Internet, although some travel is occasionally required for meeting with customers to negotiate contracts and renewals of contracts, as well as resolving possible disputes in invoicing for their services. Erskine operates out of rented premises and has a modest investment in equipment that is used by the consulting team. Erskine is a private company that follows ASPE and that has a calendar year end.

At the end of each year, Erskine obtains the services of an accountant to complete the annual accounting cycle of the business and prepare any year-end adjusting of journal entries, financial statements, and corporate tax returns.

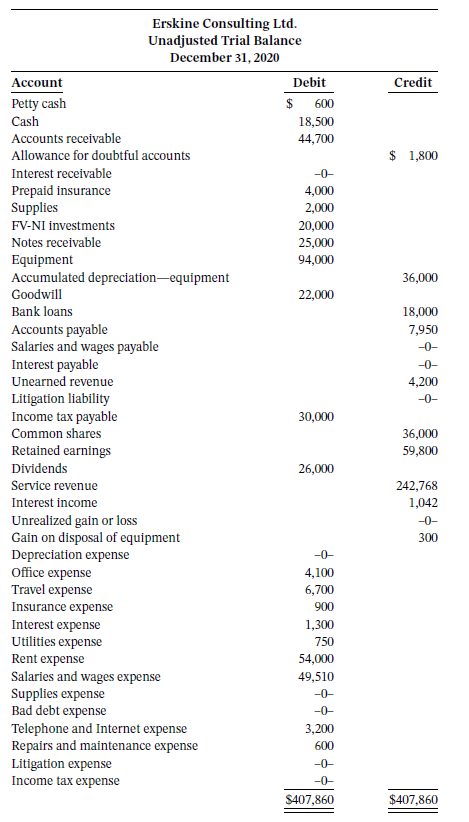

Upon arrival in early 2020, the accountant was given an unadjusted trial balance and obtained the following additional information to complete his work.

Additional information:1. Management has been going over the list of accounts receivable for possible accounts that are not collectible. One account for $700 must be written off. In the past, 5% of the balance of all accounts receivable has been the basis of an estimate for the required balance in the allowance for doubtful accounts. Management feels that this estimate should be followed for 2020.

2. After doing a count of supplies on hand, management determined that $400 of supplies remained unused at December 31, 2020.

3. The account balance in Prepaid Insurance of $4,000 represents the annual cost of the renewal of all of Erskine’s insurance policies that expire in one year. The policies’ coverage started April 1, 2020.

4. FV-NI Investments are long-term investments. The fair value of the portfolio of investments was $22,500 at December 31, 2020, based on quoted market values on the TSX.

5. In January 2020, some old equipment was sold for proceeds of $300 cash. The entry made when depositing the cash was debit Cash, credit Gain on Disposal of Equipment. The original cost of the equipment was $4,300 and the accumulated depreciation was $4,200.

6. The depreciation expense for the remaining equipment was calculated to be $7,200 for the 2020 fiscal year.

7. The notes receivable from customers are due October 31, 2023, and bear interest at 5%, with interest paid semi-annually. The last interest collected related to the notes was for the six months ended October 31, 2020.

8. Bank loans are demand bank loans for working capital needs and vary in amount as the needs arise.

The bank advised that the interest charge for December 2020 that will go through on the January 2021 bank statement is in the amount of $200.

9. Unpaid salaries and wages at December 31, 2020, totalled $790. These will be paid as part of the first payroll of 2021.

10. After some analysis, management informs the accountant that the Unearned Revenue account should have a balance of $1,000.

11. Erskine was sued by one of its former clients for $50,000 for giving bad advice and instructions. Upon discussion with legal counsel, it has been agreed that it will likely take $5,000 to settle this dispute out of court, in the next fiscal year. No entry has yet been recorded.

12. The accountant is told that a sublet lease arrangement for some excess office space has been negotiated and signed. It will provide Erskine with rent revenue starting on February 1, 2021, at a rate of $400 per month.

13. Erskine has been making income tax instalments as required by the Canada Revenue Agency. All instalment payments have been debited to the Income Taxes Payable account.14. After recording all of the necessary adjustments and posting to the general ledger, management drafted a new trial balance to arrive at the income before income taxes. Using this result, the accountant prepared the tax returns, and determined that a tax rate of 28% needed to be applied to the income before income tax amount. The necessary adjusting entry for taxes has not yet been recorded.

Instructions

a. Prepare all necessary adjusting and correcting entries required based on the information given, up to item 13.

b. Post the journal entries in adjustment columns and arrive at an adjusted trial balance. Enter the journal entries in the following worksheet format:

c. Using the adjusted trial balance columns of your worksheet, calculate the amount of income before income taxes. Use the information provided in item 14 to record income tax expense for the year.

d. Prepare a single-step statement of income, a statement of retained earnings, and a statement of financial position for 2020.

e. Explain the various levels of input in the fair value hierarchy. Based on the IFRS 13 guidance, indicate at which level in the fair value hierarchy the FV-NI investments will fall (level 1, 2, or 3). Explain your choice. How would your analysis change under ASPE? Is the amount reported in the unadjusted trial balance of $20,000 equal to the cost of the investments in the portfolio? Explain.

f. Calculate the current ratio and the payout ratio.

Step by Step Answer:

Part A Journal Entries Required Prepare all necessary adjusting and correcting entries required based on the information given up to item 13 Instruction Prepare the journal entries in the space provid...View the full answer

Intermediate Accounting Volume 1

ISBN: 978-1119496496

12th Canadian edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Irene M. Wiecek, Bruce J. McConomy