Question: West Limited reported the following amounts and information for four years ended on December 31 as follows: Deferred tax relating to property, plant, and equipment

West Limited reported the following amounts and information for four years ended on December 31 as follows:

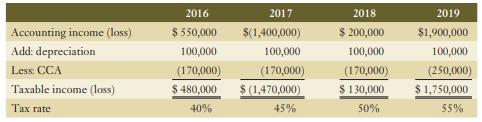

Deferred tax relating to property, plant, and equipment on December 31, 2015, was $200,000 Cr. This is the only tax account on the balance sheet. It relates to the difference between the undepreciated capital cost of $1,000,000 and net carrying value of $1,400,000 of depreciable assets. The taxable income in the two years prior to 2016 was $0. Assume any changes to future tax rates are not enacted until the year of the tax change. West’s management is confident that it is probable the company will be able to use the losses carried forward.

Required:

Prepare all journal entries related to income taxes for the four years from 2016 to 2019.

Accounting income (loss) Add: depreciation Less: CCA Taxable income (loss) Tax rate 2016 $ 550,000 100,000 (170,000) $ 480,000 40% 2017 $(1,400,000) 100,000 (170,000) $(1,470,000) 45% 2018 $ 200,000 100,000 (170,000) $ 130,000 50% 2019 $1,900,000 100,000 (250,000) $1,750,000 55%

Step by Step Solution

3.48 Rating (158 Votes )

There are 3 Steps involved in it

In order to prepare the journal entries for income taxes for the four years from 2016 to 2019 we wil... View full answer

Get step-by-step solutions from verified subject matter experts