Question: You have been asked by a client to review the records of Roberts Company, a small manufacturer of precision tools and machines. Your client is

You have been asked by a client to review the records of Roberts Company, a small manufacturer of precision tools and machines. Your client is interested in buying the business, and arrangements have been made for you to review the accounting records. Your examination reveals the following information.

1. Roberts Company commenced business on April 1, 2012, and has been reporting on a fiscal year ending March 31. The company has never been audited, but the annual statements prepared by the bookkeeper reflect the following income before closing and before deducting income taxes.

Year Ended Income

March 31 Before Taxes

2013 $ 71,600

2014 111,400

2015 103,580

2. A relatively small number of machines have been shipped on consignment. These transactions have been recorded as ordinary sales and billed as such. On March 31 of each year, machines billed and in the hands of consignees amounted to:

2013 $6,500

2014 none

2015 5,590

Sales price was determined by adding 25% to cost. Assume that the consigned machines are sold the following year.

3. On March 30, 2014, two machines were shipped to a customer on a C.O.D. basis. The sale was not entered until April 5, 2014, when cash was received for $6,100. The machines were not included in the inventory at March 31, 2014. (Title passed on March 30, 2014.)

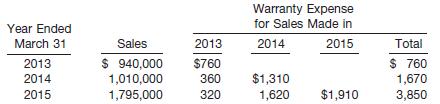

4. All machines are sold subject to a 5-year warranty. It is estimated that the expense ultimately to be incurred in connection with the warranty will amount to 1⁄2 of 1% of sales. The company has charged an expense account for warranty costs incurred.

Sales per books and warranty costs were as follows.

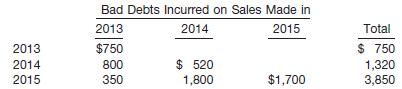

5. Bad debts have been recorded on a direct write-off basis. Experience of similar enterprises indicates that losses will approximate 1⁄4 of 1% of sales. Bad debts written off were:

6. The bank deducts 6% on all contracts financed. Of this amount, 1⁄2% is placed in a reserve to the credit of Roberts Company that is refunded to Roberts as finance contracts are paid in full. (Thus, Roberts should have a receivable for these payments and should record revenue when the net balance is remitted each year.) The reserve established by the bank has not been reflected in the books of Roberts. The excess of credits over debits (net increase) to the reserve account with Roberts on the books of the bank for each fiscal year were as follows.

2013 $ 3,000

2014 3,900

2015 5,100

$12,000

7. Commissions on sales have been entered when paid. Commissions payable on March 31 of each year were as follows.

2013 $1,400

2014 900

2015 1,120

8. A review of the corporate minutes reveals the manager is entitled to a bonus of 1% of the income before deducting income taxes and the bonus. The bonuses have never been recorded or paid.

Instructions

(a) Present a schedule showing the revised income before income taxes for each of the years ended March 31, 2013, 2014, and 2015. (Make computations to the nearest whole dollar.)

(b) Prepare the journal entry or entries you would give the bookkeeper to correct the books. Assume the books have not yet been closed for the fiscal year ended March 31, 2015. Disregard correction of income taxes.

Step by Step Solution

3.34 Rating (157 Votes )

There are 3 Steps involved in it

a Schedule of Revised Income Before Income Taxes Year Ended March 31 2013 2014 2015 Income per Books ... View full answer

Get step-by-step solutions from verified subject matter experts