You are asked to calculate the one-day 95% VaR for a portfolio using the historical method, with

Question:

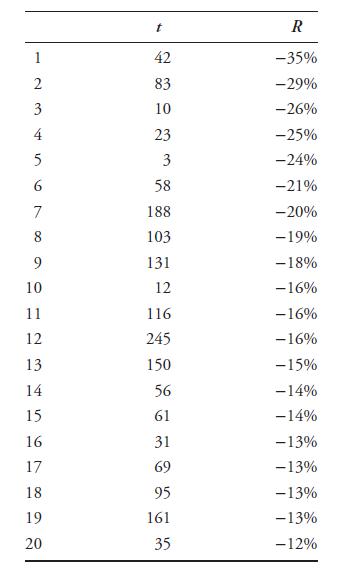

You are asked to calculate the one-day 95% VaR for a portfolio using the historical method, with a window of 256 days. The table below contains the 20 worst backcast returns for the portfolio along with the time at which the returns occurred, t = 0, 1, 2, …, 255. The most recent date is t = 0, and the oldest is t = 255.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Five percent of 256 is 128 so the 95 VaR is ...View the full answer

Answered By

Rukhsar Ansari

I am professional Chartered accountant and hold Master degree in commerce. Number crunching is my favorite thing. I have teaching experience of various subjects both online and offline. I am online tutor on various online platform.

4+ Reviews

17+ Question Solved

Related Book For

Quantitative Financial Risk Management

ISBN: 9781119522201,9781119522263

1st Edition

Authors: Michael B. Miller

Question Posted: