You have created a Monte Carlo simulation to calculate the one-day, 99% VaR of a portfolio containing

Question:

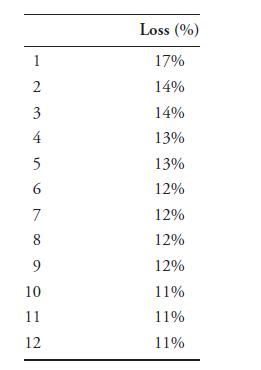

You have created a Monte Carlo simulation to calculate the one-day, 99% VaR of a portfolio containing a large number of options. In your simulation, you generate 1,000 sample one-day returns. The following table contains the 12 worst losses from your simulation. (Here, losses are represented as positive numbers, so 16% is a loss of 16% or a profit of −16%.)

What is the one-day 99% VaR? What is the one-day 99% expected shortfall?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

If we have 1000 data points in our simulation the...View the full answer

Answered By

Susan Juma

I'm available and reachable 24/7. I have high experience in helping students with their assignments, proposals, and dissertations. Most importantly, I'm a professional accountant and I can handle all kinds of accounting and finance problems.

15+ Reviews

45+ Question Solved

Related Book For

Quantitative Financial Risk Management

ISBN: 9781119522201,9781119522263

1st Edition

Authors: Michael B. Miller

Question Posted: