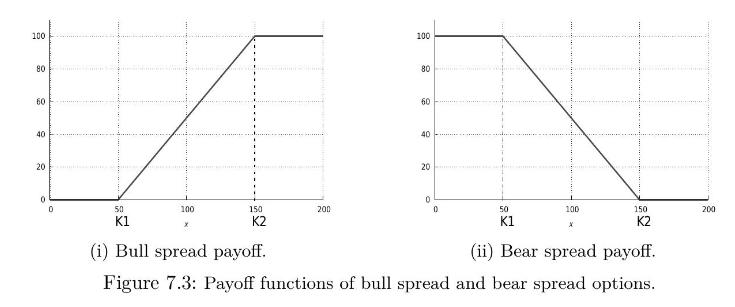

The following two graphs describe the payoff functions (phi) of bull spread and bear spread options with

Question:

The following two graphs describe the payoff functions \(\phi\) of bull spread and bear spread options with payoff \(\phi\left(S_{N}ight)\) on an underlying asset priced \(S_{N}\) at maturity time \(N\).

Data from Figure 7.3

a) Show that in each case (i) and (ii) the corresponding option can be realized by purchasing and/or short selling standard European call and put options with strike prices to be specified.

b) Price the bull spread option in cases (i) and (ii) using the Black-Scholes formula.

An option with payoff \(\phi\left(S_{T}ight)\) is priced \(\mathrm{e}^{-r T} \mathbb{E}^{*}\left[\phi\left(S_{T}ight)ight]\) at time 0 . The payoff of the European call (resp. put) option with strike price \(K\) is \(\left(S_{T}-Kight)^{+}\), resp. \(\left(K-S_{T}ight)^{+}\).

Step by Step Answer:

a i The bull spread option can be realized by purchasing one European call option with strike price ...View the full answer

Introduction To Stochastic Finance With Market Examples

ISBN: 9781032288277

2nd Edition

Authors: Nicolas Privault