Question: After completing a training course at a technical college, Michael Faraday set up in business as a self-employed electrician on 1 January 20X5. He was

After completing a training course at a technical college, Michael Faraday set up in business as a self-employed electrician on 1 January 20X5.

He was very competent at his job, but had no idea how to maintain proper accounting records.

Sometime during 20X5 one of his friends asked Michael how well his business was doing. He replied

‘All right . . . I think . . . but I’m not quite sure’.

In the ensuing conversation his friend asked whether he had prepared financial statements yet, covering his first quarter’s trading, to which Michael replied that he had not. His friend then stressed that, for various reasons, it was vital for financial statements of businesses to be prepared properly.

Shortly afterwards Michael came to see you to ask for your help in preparing financial statements for his first quarter’s trading. He brought with him, in a cardboard box, the only records he had, mainly scribbled on scraps of paper.

He explained that he started his business with a car worth £700 and £2,250 in cash, of which £250 was his savings and £2,000 had been borrowed from a relative at an interest rate of 10 per cent per annum. It was his practice to pay his suppliers and expenses in cash, to require his customers to settle their accounts in cash, and to bank any surplus in a business bank account. He maintained lists of cash receipts and cash payments, of supplies obtained on credit and of work carried out for customers and of appliances sold, on credit.

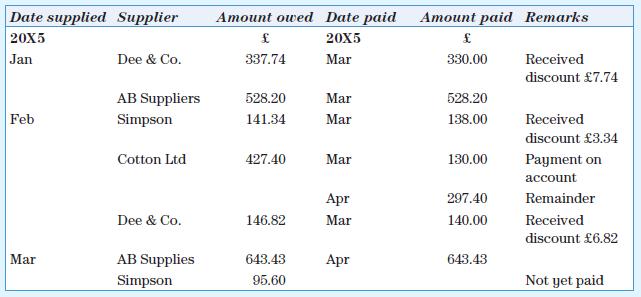

The list of credit suppliers comprised:

The purchase in January from Dee & Co. was of tools and equipment to enable him to carry out electrical repair work. All the remaining purchases were of repair materials, except for the purchase in February from Cotton Ltd, which consisted entirely of electrical appliances for resale.

In addition to the above credit transactions, he had bought repair materials for cash, as follows:

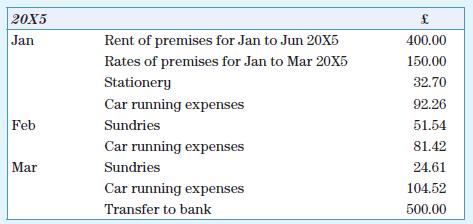

Other cash payments comprised:

He had also withdrawn £160.00 in cash at the end of each month for living expenses.

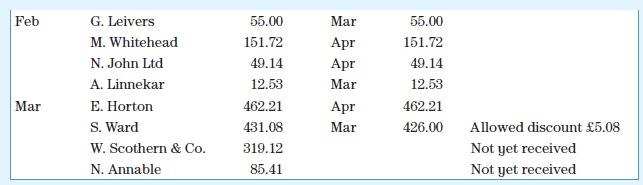

The list of credit customers comprised:

The above amounts relate to charges for repair work which he had carried out, except that the amounts shown in February for G. Leivers, N. John Ltd and A. Linnekar are for sales of electrical appliances.

In addition to the above credit transactions, he had cash takings, as follows:

He estimated that, at the end of March 20X5, his inventory of electrical repair materials was £691.02 and of electrical appliances for resale was £320.58, his tools and equipment were worth £300.00 and his car was worth £600.00.

Apart from loan interest, the only accrual was for heating and lighting, £265.00.

Required

a. Prepare:

i. Purchase day book with analysis columns for each type of purchase; and

ii. Sales day book with analysis columns for each class of business undertaken.

b. Open, post to 31 March 20X5 only, and balance a columnar cash book suitably analysed to facilitate ledger postings.

c. Open, post to 31 March 20X5 only, and balance a purchases ledger control account and a sales ledger control account. Use the closing balances in your answer to (f) below. (NB: Individual accounts for credit suppliers and credit customers are not required.)

d. Open, post and balance sales and cost of sales accounts, each with separate columns for ‘Repairs’

and ‘Appliances’.

e. Prepare M. Faraday’s statement of profit or loss for the quarter ended 31 March 20X5, distinguishing between gross profit on repairs and on appliance sales.

f. Prepare M. Faraday’s statement of financial position as at 31 March 20X5.

Date supplied Supplier 20X5 Jan Feb Mar Dee & Co. AB Suppliers Simpson Cotton Ltd Dee & Co. AB Supplies Simpson Amount owed Date paid 20X5 Mar 337.74 528.20 141.34 427.40 146.82 643.43 95.60 Mar Mar Mar Apr Mar Apr Amount paid Remarks 330.00 528.20 138.00 130.00 297.40 140.00 643.43 Received discount 7.74 Received discount 3.34 Payment on account Remainder Received discount 6.82 Not yet paid

Step by Step Solution

3.42 Rating (165 Votes )

There are 3 Steps involved in it

The question appears to be incomplete as there is no information provided on some of the cash receipts and payments details specific details on the sa... View full answer

Get step-by-step solutions from verified subject matter experts