Question: Consider the simple linear regression model where i 's are independent N(0, 2 ) random variables. Therefore, Y i is a normal random variable

Consider the simple linear regression model

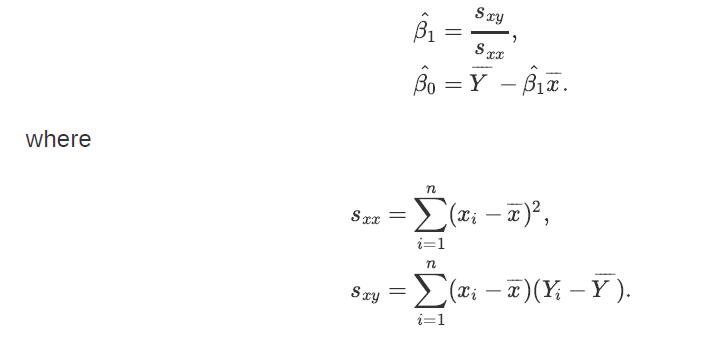

where ϵi's are independent N(0,σ2) random variables. Therefore, Yi is a normal random variable with mean β0 +β1xi and variance σ2. Moreover, Yi's are independent. As usual, we have the observed data pairs (x1, y1), (x2, y2), ⋯, (xn, yn) from which we would like to estimate β0 and β1. In this chapter, we found the following estimators

![a. Show that B is a normal random variable. b. Show that is an unbiased estimator of 3, i.e., E[81] =B. c.](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1698/3/0/8/314653a20da633eb1698308312683.jpg)

Y = Bo + Bixi + i,

Step by Step Solution

★★★★★

3.37 Rating (163 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock