Question: Let W(t) be a standard Brownian motion. Let a > 0. Define Ta as the first time that W(t) = a. That is a. Show

Let W(t) be a standard Brownian motion. Let a > 0. Define Ta as the first time that W(t) = a. That is![]()

a. Show that for any t ≥ 0, we have![]()

b. Using Part (a), show that![P(Ta t)=21-0 a (+7)] t](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1698/3/9/4/413653b712dbd55b1698394413371.jpg)

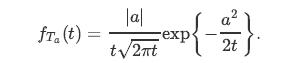

c. Using Part (b), show that the PDF of Ta is given by

By symmetry of Brownian motion, we conclude that for any a ≠ 0, we have

Ta = min{t: W(t) = a}.

Step by Step Solution

★★★★★

3.38 Rating (154 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock