Consider the simultaneous equations model, where (x) is exogenous. Assume that (Eleft(e_{i 1} mid mathbf{x}_{1} ight)=Eleft(e_{i 2}

Question:

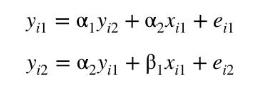

Consider the simultaneous equations model, where \(x\) is exogenous.

Assume that \(E\left(e_{i 1} \mid \mathbf{x}_{1}\right)=E\left(e_{i 2} \mid \mathbf{x}_{1}\right)=0, \operatorname{var}\left(e_{i 1} \mid \mathbf{x}_{1}\right)=\sigma_{1}^{2}, \operatorname{var}\left(e_{i 2} \mid \mathbf{x}_{1}\right)=\sigma_{2}^{2}\), and \(\operatorname{cov}\left(e_{i 1}, e_{i 2} \mid \mathbf{x}_{1}\right)=\sigma_{12}\).

a. Substitute the second equation into the first and find the reduced-form equation for \(y_{i 1}\).

b. Multiply the reduced-form equation for \(y_{i 1}\) from part (a) by \(e_{i 2}\) and find \(\operatorname{cov}\left(y_{i 1}, e_{i 2} \mid \mathbf{x}_{1}\right)=\) \(E\left(y_{i 1} e_{i 2} \mid \mathbf{x}_{1}\right)\).

c. Show that \(\operatorname{cov}\left(y_{i 1}, e_{i 2} \mid \mathbf{x}_{1}\right)=0\) if \(\alpha_{1}=0\) and \(\sigma_{12}=0\). Such a system is said to be recursive.

d. Is the OLS estimator of the first equation consistent under the conditions in (c)? Explain.

e. Is the OLS estimator of the second equation consistent under the conditions in (c)? Explain.

Step by Step Answer:

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim