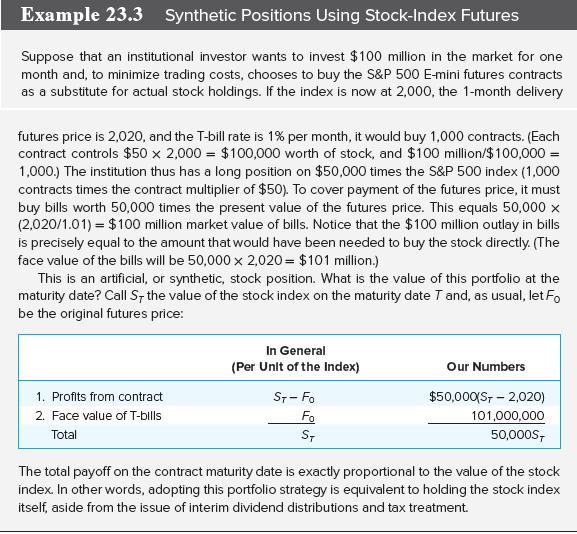

The market timing strategy of Example 23.3 also can be achieved by an investor who holds an

Question:

The market timing strategy of Example 23.3 also can be achieved by an investor who holds an indexed stock portfolio and “synthetically exits” the position using futures if and when he turns pessimistic concerning the market. Suppose the investor holds $100 million of stock (which is 50,000 times the current value of the index).

What futures position added to the stock holdings would create a synthetic T-bill exposure when he is bearish on the market? Confirm that the profits are effectively risk-free using a table like that in Example 23.3.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The net cash flow i...View the full answer

Answered By

Robert Mbae

I have been a professional custom essay writer for the last three years. Over that period of time, I have come to learn the value of focusing on the needs of the clients above everything else. With this knowledge, I have worked hard to become an acclaimed writer that can be trusted by the customers to handle the most important custom essays. I have the necessary educational background to handle projects up to the Ph.D. level. Among the types of projects that I've done, I can handle everything within Dissertations, Project Proposals, Research Papers, Term Papers, Essays, Annotated Bibliographies, and Literature Reviews, among others.

Concerning academic integrity, I assure you that you will receive my full and undivided attention through to the completion of every essay writing task. Additionally, I am able and willing to produce 100% custom writings with a guarantee of 0% plagiarism. With my substantial experience, I am conversant with all citation styles ranging from APA, MLA, Harvard, Chicago-Turabian, and their corresponding formatting. With all this in mind, I take it as my obligation to read and understand your instructions, which reflect on the quality of work that I deliver. In my paper writing services, I give value to every single essay order. Besides, whenever I agree to do your order, it means that I have read and reread your instructions and ensured that I have understood and interpreted them accordingly.

Communication is an essential part of a healthy working relationship. Therefore, I ensure that I provide the client with drafts way long before the deadline so that the customer can review the paper and comment. Upon completion of the paper writing service, the client has the time and right to review it and request any adjustments before releasing the payment.

1+ Reviews

10+ Question Solved

Related Book For

ISE Investments

ISBN: 9781260571158

12th International Edition

Authors: Zvi Bodie, Alex Kane, Alan Marcus

Question Posted: