Consider a plain vanilla interest rate swap where party A agrees to make six yearly payments to

Question:

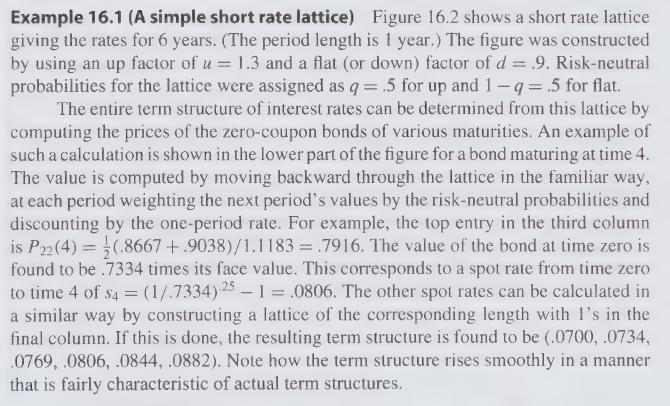

Consider a plain vanilla interest rate swap where party A agrees to make six yearly payments to party \(B\) of a fixed rate of interest on a notional principal of \(\$ 10\) million and in exchange party B will make six yearly payments to party A at the floating short rate on the same notional principal. Assume that the short rate process is described by the lattice of Example 16.1.

(a) Set up a lattice that gives the value of the floating rate cash flow stream at every short rate node, and thereby determine the initial value of this stream.

(b) What fixed rate of interest would equalize both sides of the swap?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Shem Ongek

I am a professional who has the highest levels of self-motivation. Additionally, I am always angled at ensuring that my clients get the best of the quality work possible within the deadline. Additionally, I write high quality business papers, generate quality feedback with more focus being on the accounting analysis. I additionally have helped various students here in the past with their research papers which made them move from the C grade to an A-grade. You can trust me 100% with your work and for sure I will handle your papers as if it were my assignment. That is the kind of professionalism that I swore to operate within. I think when rating the quality of my work, 98% of the students I work for always come back with more work which therefore makes me to be just the right person to handle your paper.

174+ Reviews

426+ Question Solved

Related Book For

Question Posted: