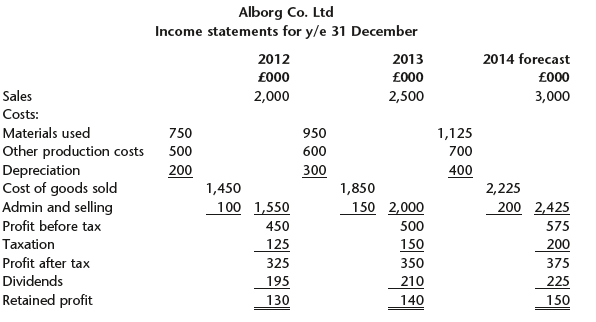

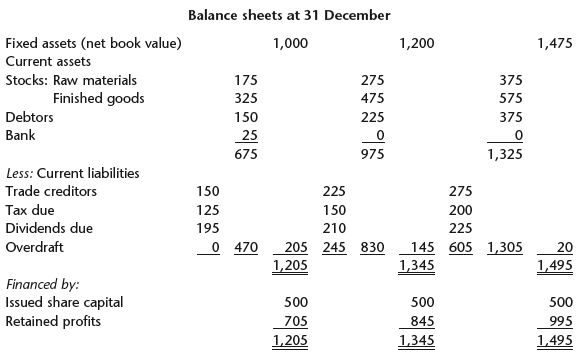

The Alborg Company Ltd manufactures and sells doors and window frames to the building trade. It has

Question:

Tasks:

1. Using a cash fl ow statement for 2013, explain why the cash position has deteriorated during that year.

2. Comment on the company€™s management of working capital by commenting on the operating and cash cycles for all three years and suggest ways in which the company might improve its working capital position. (You are aware that the 2012 position is typical of the industry in which Alborg operates.)

3 By looking at your suggestions to improve working capital and at the expected cash flow over the next three months, advise the company how (if at all) the overdraft can be reduced to £125,000 by the end of March 2014.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Q1 Cash Flow Statement 2007 000 Profit before tax 500 Add back Depreciation 300 RM Stock increase 100 FG Stock increase 150 Debtor increase 75 Creditor increase 75 Subtotal 550 Dividend paid 195 Tax p...View the full answer

Answered By

Fahmin Arakkal

Tutoring and Contributing expert question and answers to teachers and students.

Primarily oversees the Heat and Mass Transfer contents presented on websites and blogs.

Responsible for Creating, Editing, Updating all contents related Chemical Engineering in

latex language

8+ Reviews

22+ Question Solved

Related Book For

Managerial Accounting Decision Making and Performance Management

ISBN: 978-0273764489

4th edition

Authors: Ray Proctor

Question Posted: