Stewart Co.s beginning inventory and purchases during the year ended December 31, 20Y2, were as follows: Instructions

Question:

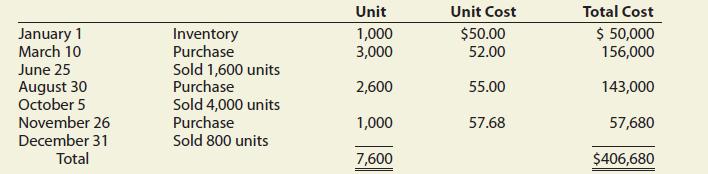

Stewart Co.’s beginning inventory and purchases during the year ended December 31, 20Y2, were as follows:

Instructions 1. Determine the cost of inventory on December 31, 20Y2, using the perpetual inventory system and each of the following inventory costing methods:

a. first-in, first-out

b. last-in, first-out

c. weighted average (round weighted average cost per unit to two decimal places)

2. Determine the cost of inventory on December 31, 20Y2, using the periodic inventory system and each of the following inventory costing methods:

a. first-in, first-out

b. last-in, first-out

c. weighted average cost (round weighted average cost per unit to two decimal places)

3. (Appendix) Assume that during the fiscal year ended December 31, 20Y2, sales were $530,000 and the estimated gross profit rate was 36%. Estimate the ending inventory at December 31, 20Y2, using the gross profit method.

Step by Step Answer:

1 a Firstin firstout method 68680 11000 57680 b Lastin firstout me...View the full answer

Financial And Managerial Accounting

ISBN: 9781337902663

15th Edition

Authors: Carl S. Warren, Jefferson P. Jones, William B. Tayler