A continuously exponential averaged arithmetic Asian option is a contract, where the average price of the underlying

Question:

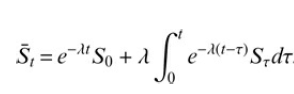

A continuously exponential averaged arithmetic Asian option is a contract, where the average price of the underlying is computed as

The parameter ? ? 0 is an arbitrary weight factor. Rewrite the averaging condition in differential form and explain the effect of the parameter ?.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To rewrite the averaging condition in differential form we differentiate the exponential average pri...View the full answer

Answered By

Atavali Ramesh

My self Arya, always ready for your challenges in Maths, Science & all of the Arts subjects

(Best experience in: Trading and Crypto Trading)

0 Reviews

10+ Question Solved

Related Book For

Question Posted: