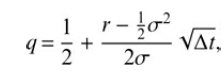

In demonstrating the transition from the binomial model to the Black?Scholesmodel, the parametrization u/d = e ????t

Question:

In demonstrating the transition from the binomial model to the Black?Scholesmodel, the parametrization u/d = e????t chosen in step 3, with ?t = ?/T.?Show that the martingale principle results in the same risk-neutral probability?

if the u/d-parametrization is Taylor-expanded to second order.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The mart ing ale principle states that the expected return of a risky asset is equal t...View the full answer

Answered By

SHINKI JALHOTRA

I have worked with other sites like Course Hero as a tutor and I have great knowledge on IT skills.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: