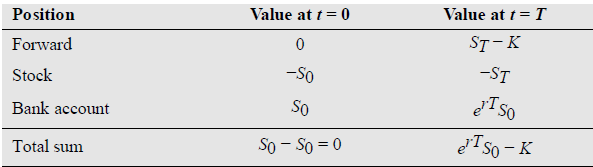

Use an arbitrage argument, analogous to the one in Table 11.1 on page 212, to prove that

Question:

Use an arbitrage argument, analogous to the one in Table 11.1 on page 212, to prove that in a stochastic interest rate world, the strike price of a forward contract Ft(K, T) that can be entered costlessly at time t = 0 has to be

which is the forward price of a non-dividend paying underlying V at t = 0.

Table 11.1 Forward arbitrage portfolio

In finance, the strike price of an option is the fixed price at which the owner of the option can buy, or sell, the underlying security or commodity.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

ANSWER In a stochastic interest rate world the forward price of a nondividend paying underlying asse...View the full answer

Answered By

Akash M Rathod

I have been utilized by educators and students alike to provide individualized assistance with everything from grammar and vocabulary to complex problem-solving in various academic subjects. I can provide explanations, examples, and practice exercises tailored to each student's individual needs, helping them to grasp difficult concepts and improve their skills.

My tutoring sessions are interactive and engaging, utilizing a variety of tools and resources to keep learners motivated and focused. Whether a student needs help with homework, test preparation, or simply wants to improve their skills in a particular subject area, I am equipped to provide the support and guidance they need to succeed.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: