Consider the family of forward swap rates K t [T i ,T n ],i = 0, 1,

Question:

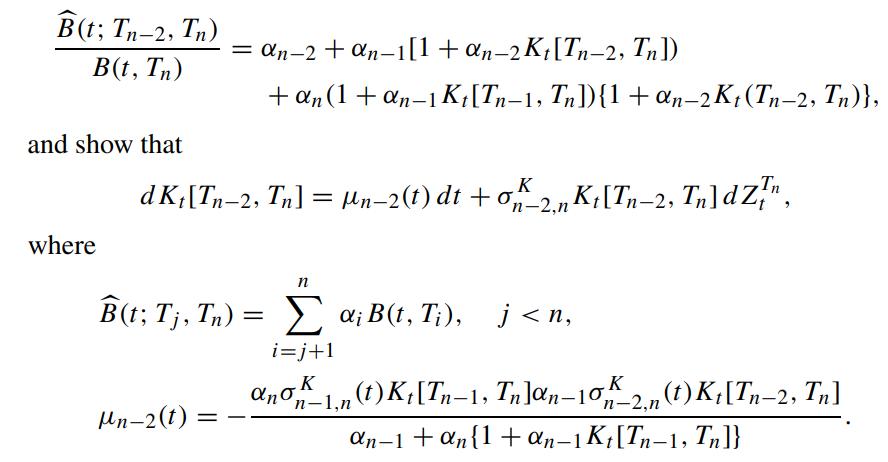

Consider the family of forward swap rates Kt[Ti,Tn],i = 0, 1, ··· ,n−1, with the common terminal payment date Tn. We would like to express the dynamics of Kt[Ti,Tn] under the terminal forward measure QTn . Since Kt[Tn−1,Tn] is simply the LIBOR Ln−1(t), we have

![dK:[Tn1,Tn] dLn-1(t) Ki[Tn1, Tn] Ln-1(t) = K = 0, -1,n(t) dz[n,](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/6/5/0/776655ddf185e0de1700650776778.jpg) where ZtTn is QTn -Brownian. Derive the relation

where ZtTn is QTn -Brownian. Derive the relation

In general, deduce the relation

![B(t; Ti , Tn) B(t, Th) k + (1 + a; K,[T;, Th]), k=i+1 j=i+1 i = n 2, n 3, ..., 0, = ; +](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/6/5/0/860655ddf6c882961700650861015.jpg)

and express the dynamics of Kt[Ti,Tn] under the terminal measure QTn.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The given relations involve forward swap rates KT T with the common terminal payment date T and the ...View the full answer

Answered By

Muhammad Umair

I have done job as Embedded System Engineer for just four months but after it i have decided to open my own lab and to work on projects that i can launch my own product in market. I work on different softwares like Proteus, Mikroc to program Embedded Systems. My basic work is on Embedded Systems. I have skills in Autocad, Proteus, C++, C programming and i love to share these skills to other to enhance my knowledge too.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: