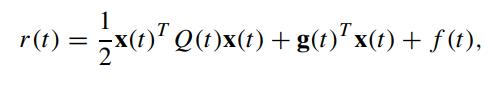

Consider the following general formulation of the quadratic term structure model (Jamshidian, 1996), where the short rate

Question:

Consider the following general formulation of the quadratic term structure model (Jamshidian, 1996), where the short rate is defined by

for some smooth deterministic vector α(t), matrices β(t) and σ(t).

for some smooth deterministic vector α(t), matrices β(t) and σ(t).

(a) Show that the governing partial differential equation for the price of a contingent claim C(x,t) is given by

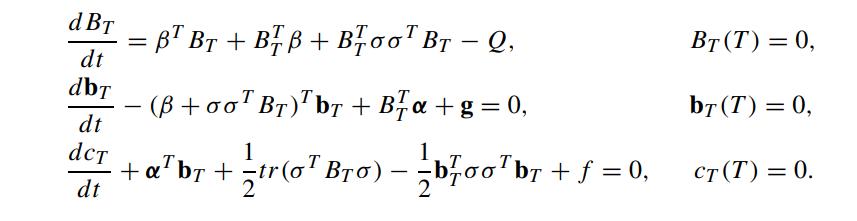

(b) Show that the price of a T -maturity discount bond admits the following exponential affine form

where the matrix BT (t), vector bT (t) and scalar cT (t) are governed by the following coupled system of ordinary differential equations:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Mamba Dedan

I am a computer scientist specializing in database management, OS, networking, and software development. I have a knack for database work, Operating systems, networking, and programming, I can give you the best solution on this without any hesitation. I have a knack in software development with key skills in UML diagrams, storyboarding, code development, software testing and implementation on several platforms.

49+ Reviews

119+ Question Solved

Related Book For

Question Posted: