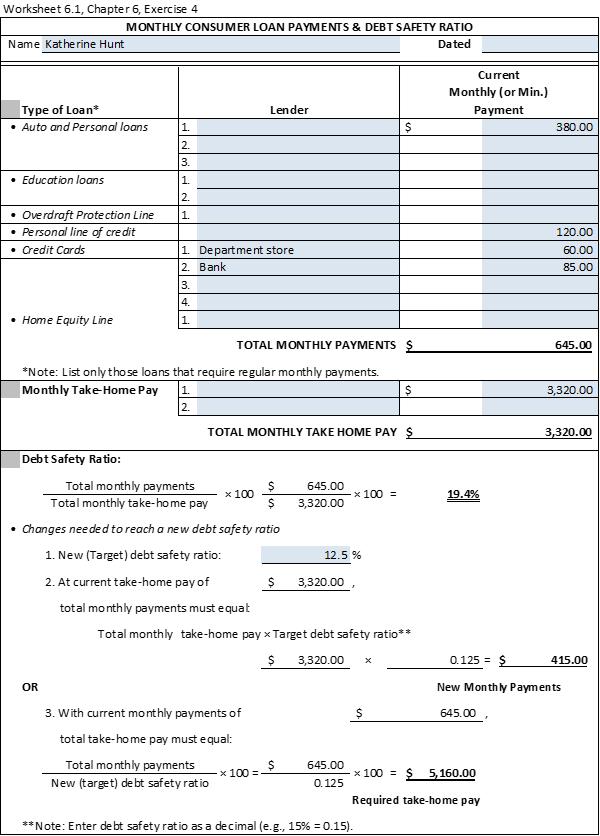

Use Worksheet 6.1. Katherine Hunt is evaluating her debt safety ratio. Her monthly take- home pay is

Question:

Use Worksheet 6.1. Katherine Hunt is evaluating her debt safety ratio. Her monthly take- home pay is $3,320. Each month, she pays $380 for an auto loan, $120 on a personal line of credit, $60 on a department store charge card, and $85 on her bank credit card. Complete Worksheet 6.1 by listing Katherine’s outstanding debts, and then calculate her debt safety ratio. Given her current take-home pay, what is the maximum amount of monthly debt payments that Katherine can have if she wants her debt safety ratio to be 12.5 percent? Given her current monthly debt payment load, what would Katherine’s take-home pay have to be if she wanted a 12.5 percent debt safety ratio?

Step by Step Answer:

K atherine Hunt s Out standing Deb ts Auto Loan 380 Personal Line of Credit 120 D...View the full answer

Personal Financial Planning

ISBN: 9780357438480

15th Edition

Authors: Randy Billingsley, Lawrence J. Gitman, Michael D. Joehnk