Question: 2.1. Let X X,, . . . be independent identically distributed positive random variables whose common distribution function is F. We interpret X X ...

2.1. Let X X,, . . . be independent identically distributed positive random variables whose common distribution function is F. We interpret X X ... as successive bids on an asset offered for sale. Suppose that the policy is followed of accepting the first bid that exceeds some prescribed number A. Formally, the accepted bid is X,, where N= min{k? 1;Xk>A}.

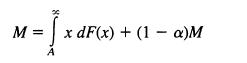

Set a = Pr(X, > A) and M = E[X,,,].

(a) Argue the equation

by considering the possibilities, either the first bid is accepted, or it is not.

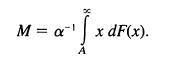

(b) Solve for M, thereby obtaining

(c) When X, has an exponential distribution with parameter A, use the memoryless property to deduce M = A + A'.

(d) Verify this result by calculation in (b).

M =S xdF(x) (1)M

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts