1. A change in accounting principle from one that is not generally accepted to one that is...

Question:

1. A change in accounting principle from one that is not generally accepted to one that is generally accepted should be treated as

a) An error and corrected by prior period adjustment

b) A change in accounting principle and the cumulative effect included in net income

c) A change in accounting principle and prior period financial statements are restated

d) A change in accounting principle and adjustments made prospectively

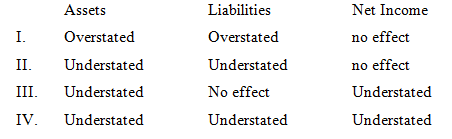

2. The December 31, 2010, ending inventory failed to include $10,000 of inventory that was received on December 27, 2010. The purchase on account was, however, properly recorded on the date of delivery. What effect will this error have on the December 31, 2010, assets, liabilities, and net income for the year then ended?

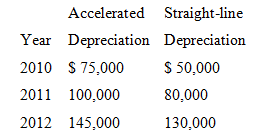

3. The Zack Company began its operations on January 1, 2010, and used an accelerated method of depreciation for its machinery and equipment. On January 1, 2012, Zack adopted the straight-line method of depreciation. The following information is available regarding depreciation expense for each method:

What is the before-tax cumulative effect on prior years' income that would be reported as of January 1, 2012, due to changing to a different depreciation method?

a) $0

b) A decrease of $45,000

c) An increase of $45,000

d) An increase of $60,000

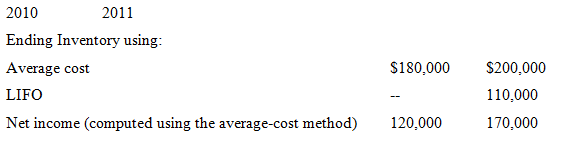

4. Wilma Company began operations in 2010 and uses the average cost method in costing its inventory. In 2011, Wilma is investigating a change to the LIFO method. Before making that determination, Wilma desires to determine what effect such a change will have on net income. Wilma has compiled the following information:

Assume a 40% tax rate.

If Wilma adopted LIFO in 2011, net income would be

a) $ 80,000

b) $116,000

c) $170,000

d) $224,000

5 Generally accepted methods of accounting for a change in accounting principle include

a) Restating prior years' financial statements presented for comparative purposes

b) Including the cumulative effect of the change in net income

c) Prospective changes

d) Making a prior period adjustment

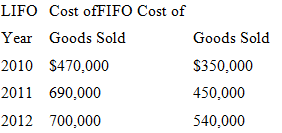

6. The Lawrence Company began its operations on January 1, 2010, and used the LIFO method of accounting for its inventory. On January 1, 2012, Lawrence Company adopted FIFO in accounting for its inventory. The following information is available regarding cost of goods sold for each method:

Assuming a tax rate of 30% and the same accounting change adopted for tax purposes, how would the effect of the accounting change be reported in opening retained earnings on the 2012 financial statements?

a. +$360,000 restatement

b. +$252,000 restatement

c. no restatement

d. ($700,000) restatement

7. A company's pension expense includes all of the following items except

a) Service cost

b) Employer's contribution to the pension fund

c) Amortization of prior service cost

d) Interest cost on the projected benefit obligation

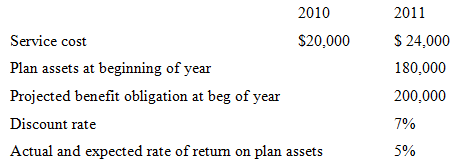

8. Given the following information

What is pension expense for 2011?

a) $24,000

b) $29,000

c) $38,000

d) $47,000

Expert Answer: