Assume that Blue Sunday Bank has $200 million of assets with an average duration of 1.6 years

Question:

Assume that Blue Sunday Bank has $200 million of assets with an average duration of 1.6 years and liabilities of $100 million with an average duration of 1.95 years. Compute the current duration gap of this bank. Assuming that U.S. Treasury bonds with a duration of 1.2 years are currently quoted in the market at 98-16, explain the position (buy of sell) in a futures contract (including the number of contracts) that the bank manager should take to eliminate interest rate risk.

The following quotes will be used for the next two parts of this problem.

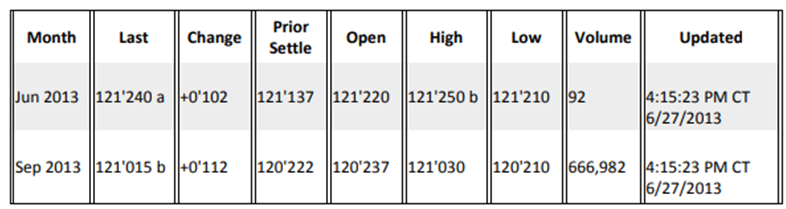

5-Year U.S. Treasury Bond Futures Contract Quotes from 6 / 27 / 2117

CBT $100,000; pts 32 nd of 100

Source: CME Group. (2013, June 27). 5-year U.S. Treasury note futures. Retrieved from http://www.cmegroup.com/trading/interest-rates/us-treasury/S-year-us-treasury-note_quotes_globex.htmIttprodType=AME

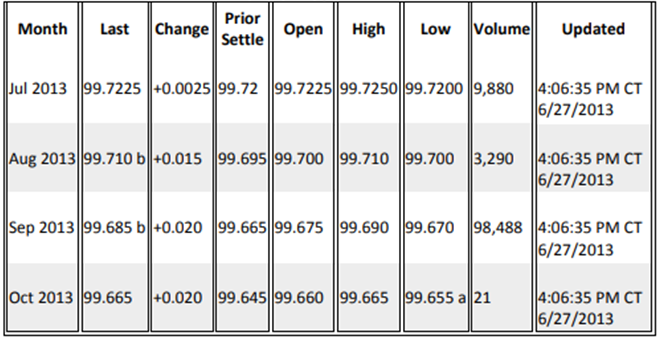

Eurodollar Future Contracts Quotes on 6/27/2013 CME - $100,000; pts of 100%

Source: CME Group. (2013, June 27). 5-year U.S. Treasury note futures. Retrieved from http://www.cmegroup.com/trading/interest-rates/us-treasury/S-year-us-treasury-note_quotes_globex.htmIttprodType=AME

Eurodollar Future Contracts Quotes on 6/27/2013 CME - $100,000; pts of 100%

Expert Answer:

Current duration gap assets duration gaptotal assetstotal liabilies total assetsaverage duration of ... View the full answer

Financial Institutions Management A Risk Management Approach

ISBN: 978-0071051590

8th edition

Authors: Marcia Cornett, Patricia McGraw, Anthony Saunders