Question: D Question 8 3 pts Assume () there are no transactions costs, (ii) the risk-free borrowing and lending rates are equal, (ili) if you lend

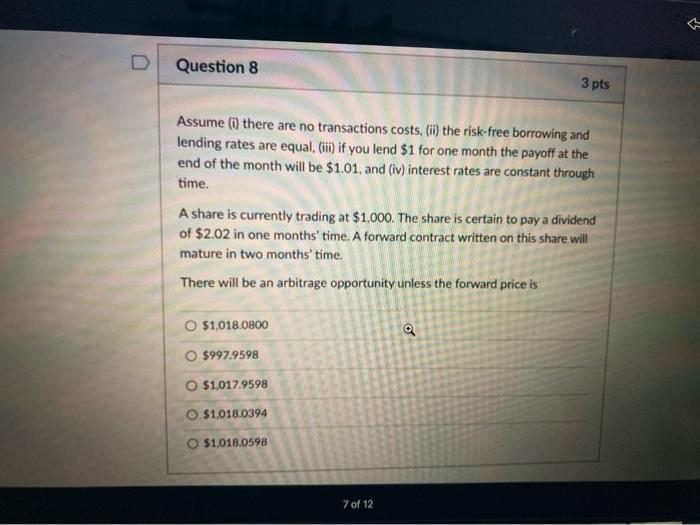

D Question 8 3 pts Assume () there are no transactions costs, (ii) the risk-free borrowing and lending rates are equal, (ili) if you lend $1 for one month the payoff at the end of the month will be $1.01, and (iv) interest rates are constant through time. A share is currently trading at $1,000. The share is certain to pay a dividend of $2.02 in one months' time. A forward contract written on this share will mature in two months' time. There will be an arbitrage opportunity unless the forward price is $1,018.0800 O $997.9598 O $1,017.9598 O.$1,018.0394 O $1,018.0598 7 of 12

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock