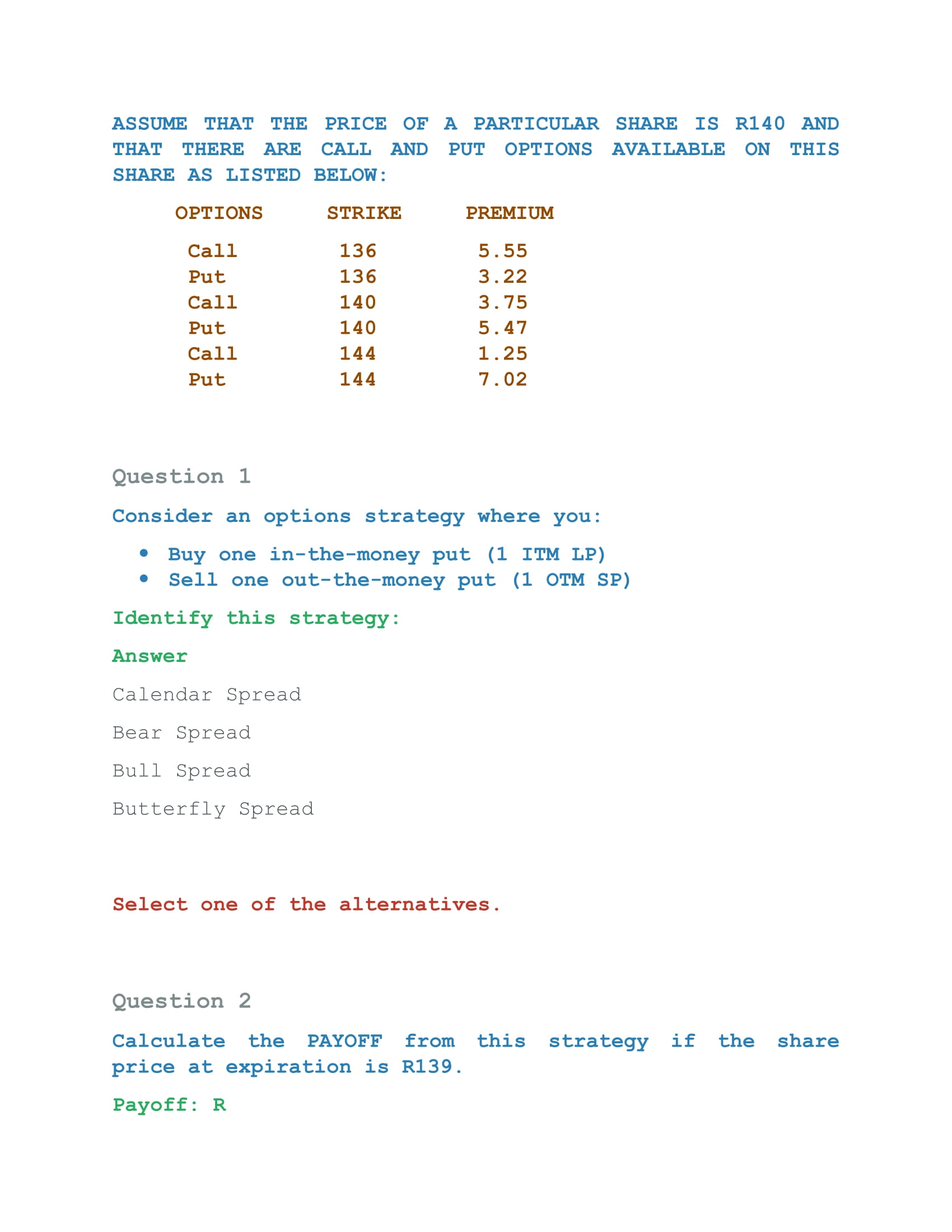

Question: ASSUME THAT THE PRICE OF A PARTICULAR SHARE IS R140 AND THAT THERE ARE CALL AND PUT OPTIONS AVAILABLE ON THIS SHARE AS LISTED BELOW:

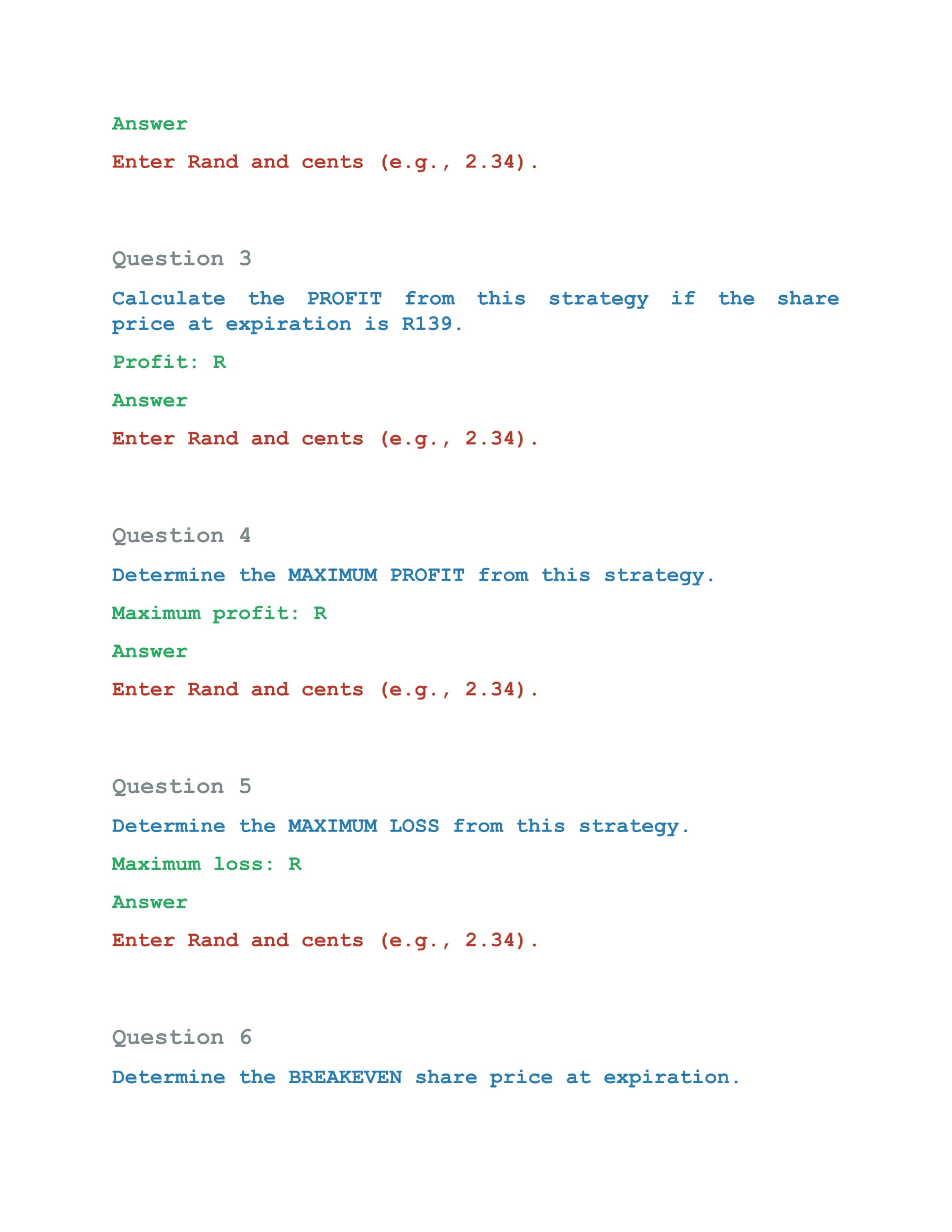

ASSUME THAT THE PRICE OF A PARTICULAR SHARE IS R140 AND THAT THERE ARE CALL AND PUT OPTIONS AVAILABLE ON THIS SHARE AS LISTED BELOW: OPTIONS Call Put Call Put Call Put Question 1 STRIKE 136 136 140 140 144 144 PREMIUM 5. .22 .75 .47 .25 .02 di'Lww 55 Consider an options strategy where you: 0 Buy one inthemoney put (1 ITM LP) 0 Sell one outthemoney put (1 OTM SP) Identify this strategy: Answer Calendar Spread Bear Spread Bull Spread Butterfly Spread Select one of the alternatives. Question 2 Calculate the PAYOFF from this price at expiration is R139. Payoff: R strategy if the share Answer Enter Rand and cents (e.g., 2.34). Question 3 Calculate the PROFIT from this strategy if the share price at expiration is R139. Profit: R Answer Enter Rand and cents (e.g., 2.34). Question 4 Determine the MAXIMUM PROFIT from this strategy. Maximum profit: R Answer Enter Rand and cents (e.g., 2.34). Question 5 Determine the MAXIMUM LOSS from this strategy. Maximum loss: R Answer Enter Rand and cents (e.g., 2.34). Question 6 Determine the BREAKEVEN share price at expiration.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts