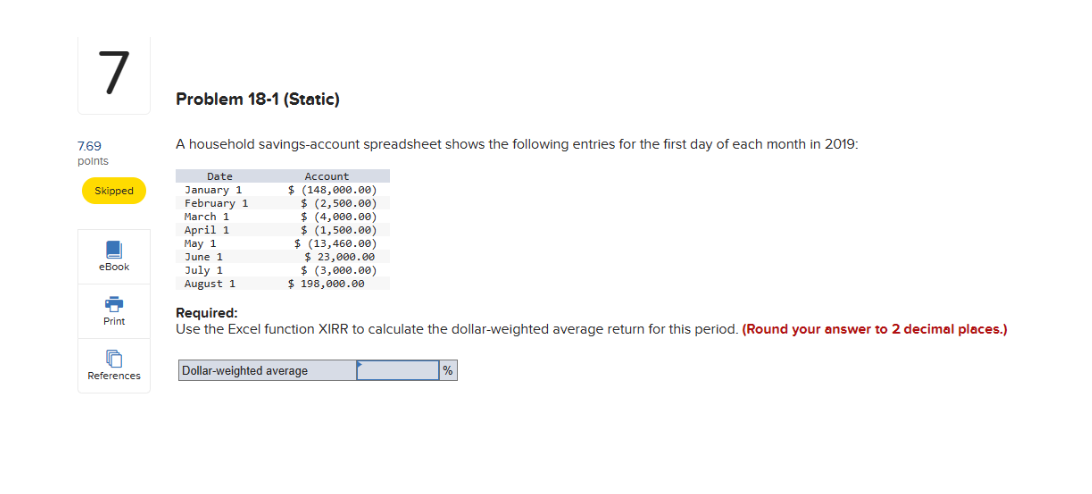

Question: 7 Problem 18-1 (Static) 7.69 A household savings-account spreadsheet shows the following entries for the first day of each month in 2019: points Date Account

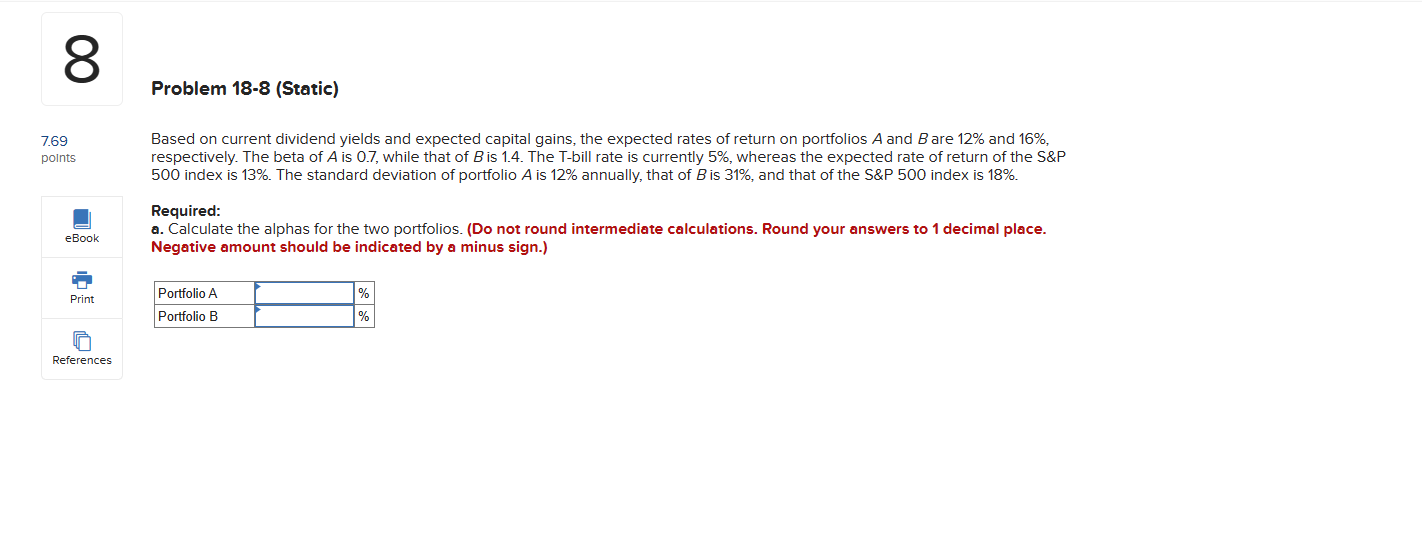

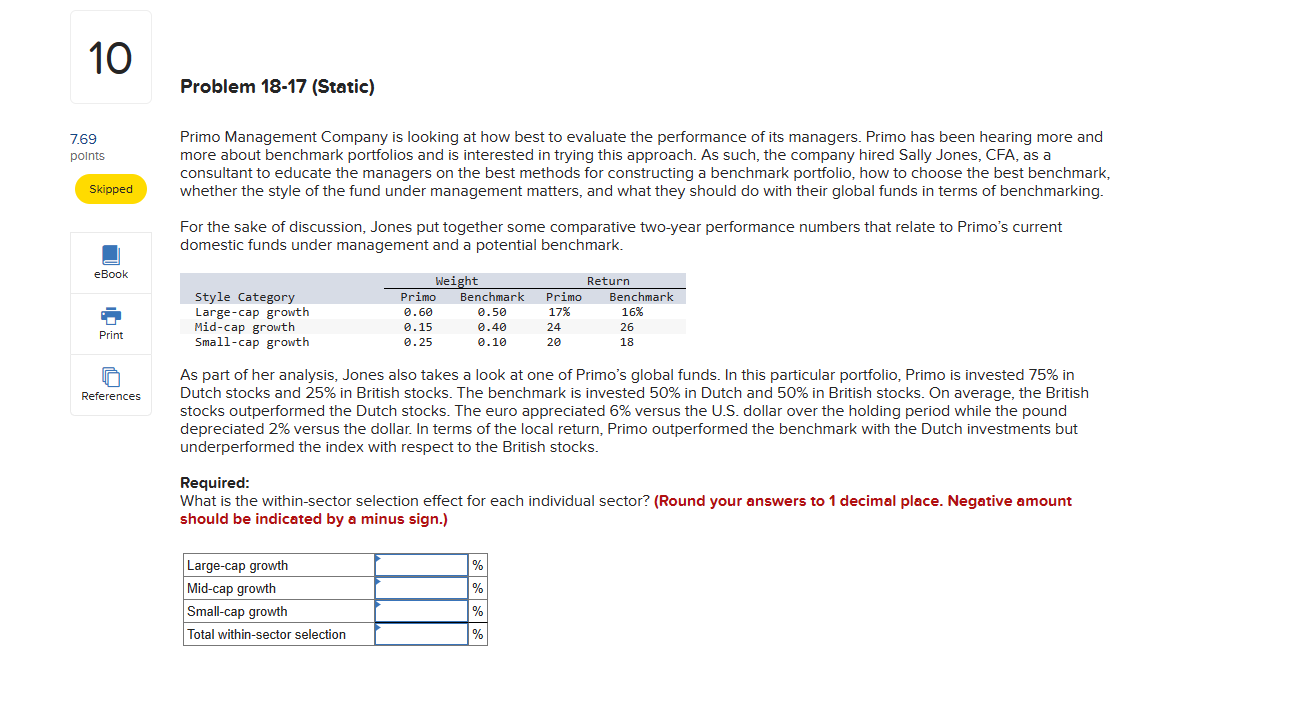

7 Problem 18-1 (Static) 7.69 A household savings-account spreadsheet shows the following entries for the first day of each month in 2019: points Date Account Skipped January 1 $ (148, 000.00) February 1 $ (2, 500.00) March 1 $ (4,000.00) April 1 $ (1, 500.00) May 1 $ (13, 460.00) June 1 $ 23,060.00 eBook July 1 $ (3,000.00) August 1 $ 198, 000.00 Required: Print Use the Excel function XIRR to calculate the dollar-weighted average return for this period. (Round your answer to 2 decimal places.) References Dollar-weighted average %3 Problem 18-8 (Static) 769 Based on current dividend yields and expected capital gains, the expected rates of return on portfolios A and B are 12% and 16%, points respectively. The beta of A is 07, while that of Bis 1.4. The T-bill rate is currently 5%, whereas the expected rate of return of the S&P 500 index is 13%. The standard deviation of portfolio A is 12% annually, that of Bis 31%, and that of the S&P 500 index is 18%. E Required: eBook a. Calculate the alphas for the two portfolios. (Do not round intermediate calculations. Round your answers to 1 decimal place. Negative amount should be indicated by a minus sign.) E Portfolio A % Portfolio B % ll_i References 10 769 points Skipped References Problem 18-17 (Static) Primo Management Company is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consultant to educate the managers on the best methods for constructing a benchmark portfolio, how to choose the best benchmark, whether the style of the fund under management matters, and what they should do with their global funds in terms of benchmarking. For the sake of discussion, Jones put together some comparative two-year performance numbers that relate to Primo's current domestic funds under management and a potential benchmark. Weight Return Style Category Primo Benchmark Primo Benchmark Large-cap growth 2.60 @.50 17% 16% Mid-cap growth 9.15 .40 24 26 Small-cap growth 9.25 @e.1e 20 18 As part of her analysis, Jones also takes a look at one of Primo's global funds. In this particular portfolio, Primo is invested 75% in Dutch stocks and 25% in British stocks. The benchmark is invested 50% in Dutch and 50% in British stocks. On average, the British stocks outperformed the Dutch stocks. The euro appreciated 6% versus the U.S. dollar over the holding period while the pound depreciated 2% versus the dollar. In terms of the local return, Primo outperformed the benchmark with the Dutch investments but underperformed the index with respect to the British stocks. Required: What is the within-sector selection effect for each individual sector? {Round your answers to 1 decimal place. Negative amount should be indicated by a minus sign.) Large-cap growth Mid-cap growth Small-cap growth Total within-sector selection

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts