Question: 00 89 Question 4 10 points 90 We will use the binonial option pricing nodel to value the following put option on a stock. 91

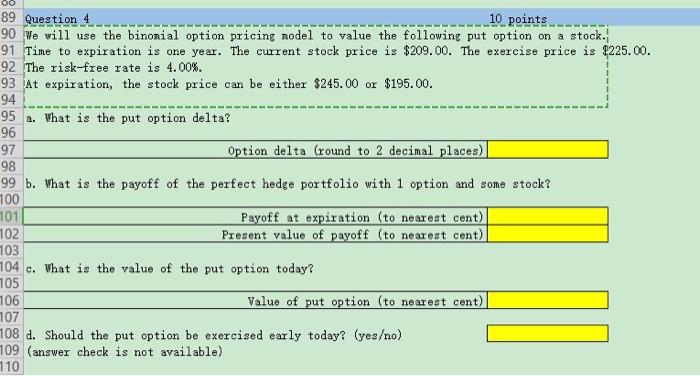

00 89 Question 4 10 points 90 We will use the binonial option pricing nodel to value the following put option on a stock. 91 Time to expiration is one year. The current stock price is $209.00. The exercise price is $225.00. 92 The risk-free rate is 4.00%. 93 At expiration, the stock price can be either $245.00 or $195.00. 94 95 a. What is the put option delta? 96 97 Option delta (round to 2 decimal places) 98 99 b. What is the payoff of the perfect hedge portfolio with 1 option and some stock? 100 101 Payoff at expiration (to nearest cent) 102 Present value of payoff (to nearest cent) 103 104 c. What is the value of the put option today? 105 106 Value of put option (to nearest cent) 107 108 d. Should the put option be exercised early today? (yeso) 709 (answer check is not available) 110

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts