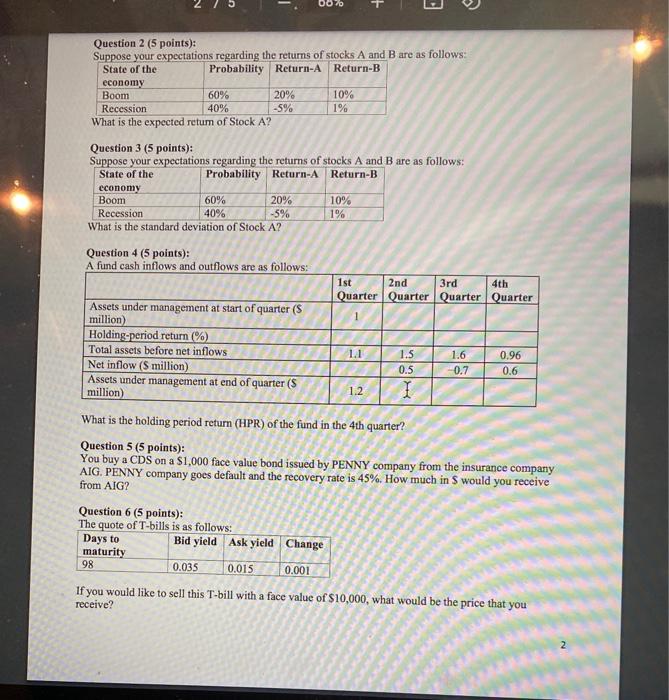

Question: 000 + > 1% Question 2 (5 points): Suppose your expectations regarding the returns of stocks A and B are as follows: State of the

000 + > 1% Question 2 (5 points): Suppose your expectations regarding the returns of stocks A and B are as follows: State of the Probability Return-A Return-B economy Boom 60% 20% 10% Recession 40% -5% What is the expected retum of Stock A? Question 3 (5 points): Suppose your expectations regarding the returns of stocks A and B are as follows: State of the Probability Return-A Return-B economy Boom 60% 20% 10% Recession 40% -5% 1% What is the standard deviation of Stock A? Question 4 (5 points): A fund cash inflows and outflows are as follows: 1st 2nd 3rd 4th Quarter Quarter Quarter Quarter Assets under management at start of quarter (S million) Holding period return (%) Total assets before net inflows Net inflow (S million) Assets under management at end of quarter (S million) 1.1 1.5 0.5 1.6 0.7 0.96 0.6 1.2 + What is the holding period return (HPR) of the fund in the 4th quarter? Question 5 (5 points): You buy a CDS on a $1,000 face value bond issued by PENNY company from the insurance company AIG, PENNY company goes default and the recovery rate is 45%. How much in S would you receive from AIG? Question 6 (5 points): The quote of T-bills is as follows: Days to Bid yield Ask yield Change maturity 98 0.035 0.015 0.001 If you would like to sell this T-bill with a face value of $10,000, what would be the price that receive? you

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts