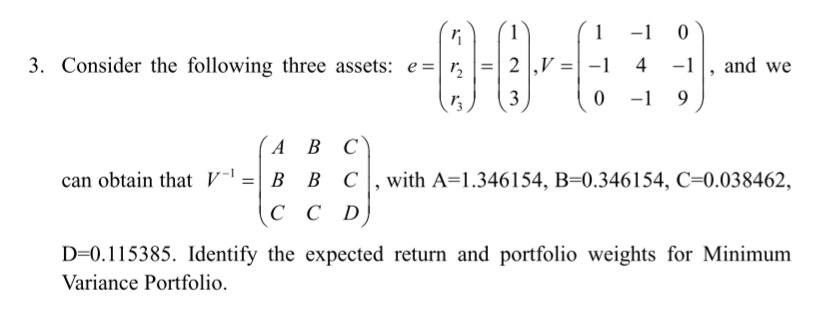

Question: 00-6 3. Consider the following three assets: e= r2 T + 1 -1 0 -1 0 -1 9 -1 and we A B C can

00-6 3. Consider the following three assets: e= r2 T + 1 -1 0 -1 0 -1 9 -1 and we A B C can obtain that v-' = B B C , with A=1.346154, B=0.346154, C=0.038462, C C D D=0.115385. Identify the expected return and portfolio weights for Minimum Variance Portfolio. 00-6 3. Consider the following three assets: e= r2 T + 1 -1 0 -1 0 -1 9 -1 and we A B C can obtain that v-' = B B C , with A=1.346154, B=0.346154, C=0.038462, C C D D=0.115385. Identify the expected return and portfolio weights for Minimum Variance Portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock