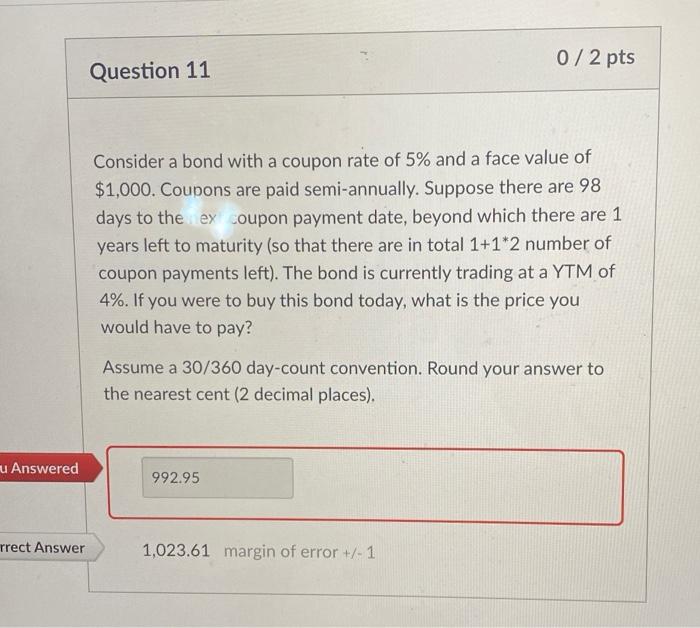

Question: 0/2 pts Question 11 Consider a bond with a coupon rate of 5% and a face value of $1,000. Coupons are paid semi-annually. Suppose there

0/2 pts Question 11 Consider a bond with a coupon rate of 5% and a face value of $1,000. Coupons are paid semi-annually. Suppose there are 98 days to the ex coupon payment date, beyond which there are 1 years left to maturity (so that there are in total 1+1*2 number of coupon payments left). The bond is currently trading at a YTM of 4%. If you were to buy this bond today, what is the price you would have to pay? Assume a 30/360 day-count convention. Round your answer to the nearest cent (2 decimal places). u Answered 992.95 rrect Answer 1,023.61 margin of error +/- 1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock