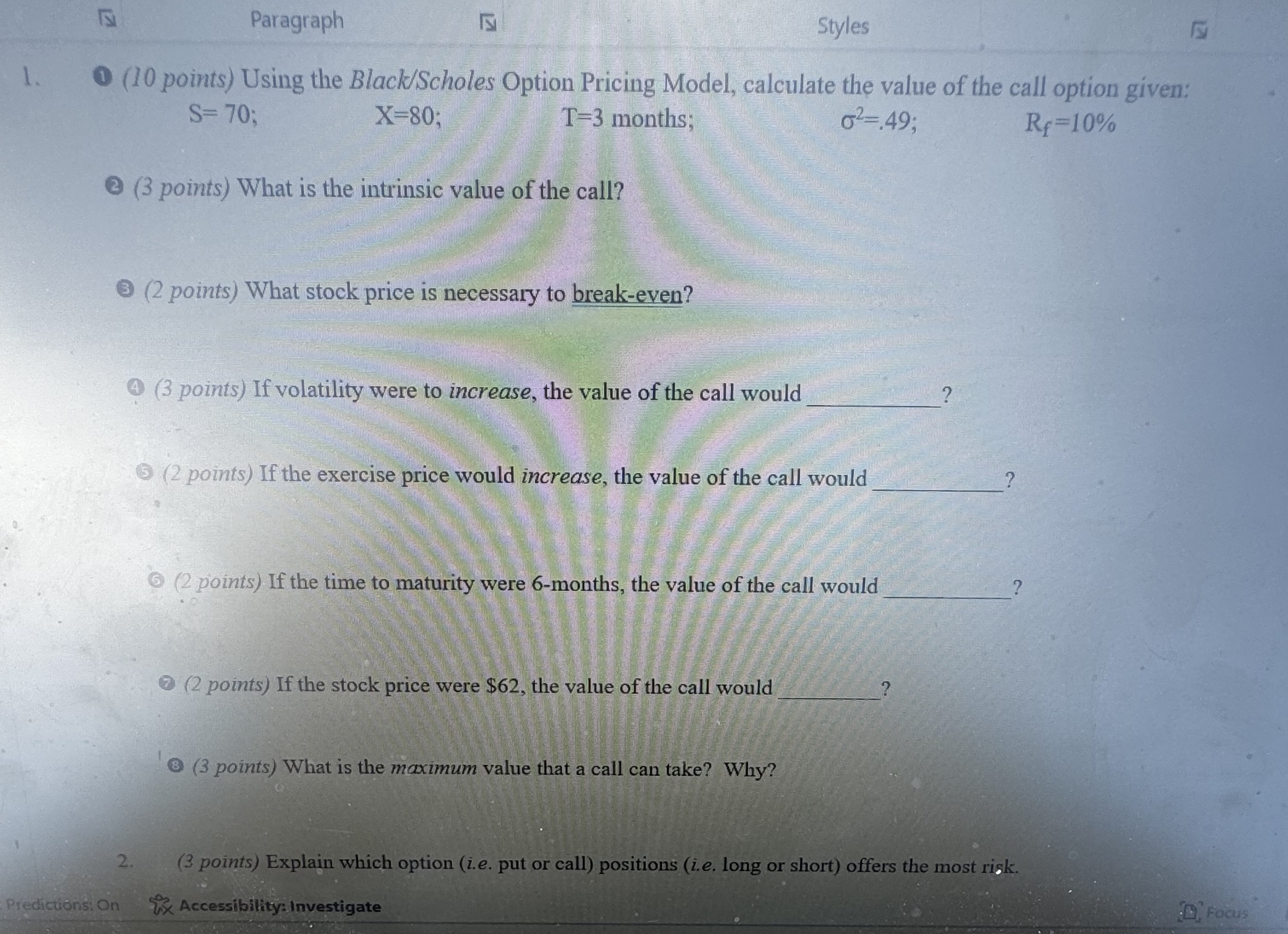

Question: ( 1 0 points ) Using the Black / Scholes Option Pricing Model, calculate the value of the call option given: S = 7 0

points Using the BlackScholes Option Pricing Model, calculate the value of the call option given:

;

;

months;

;

points What is the intrinsic value of the call?

points What stock price is necessary to breakeven?

points If volatility were to increase, the value of the call would

points If the exercise price would increase, the value of the call would

points If the time to maturity were months, the value of the call would

points If the stock price were $ the value of the call would

points What is the maximum value that a call can take? Why?

points Explain which option ie put or call positions ie long or short offers the most risk.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock