Question: 1. 2. Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium.

1.

2.

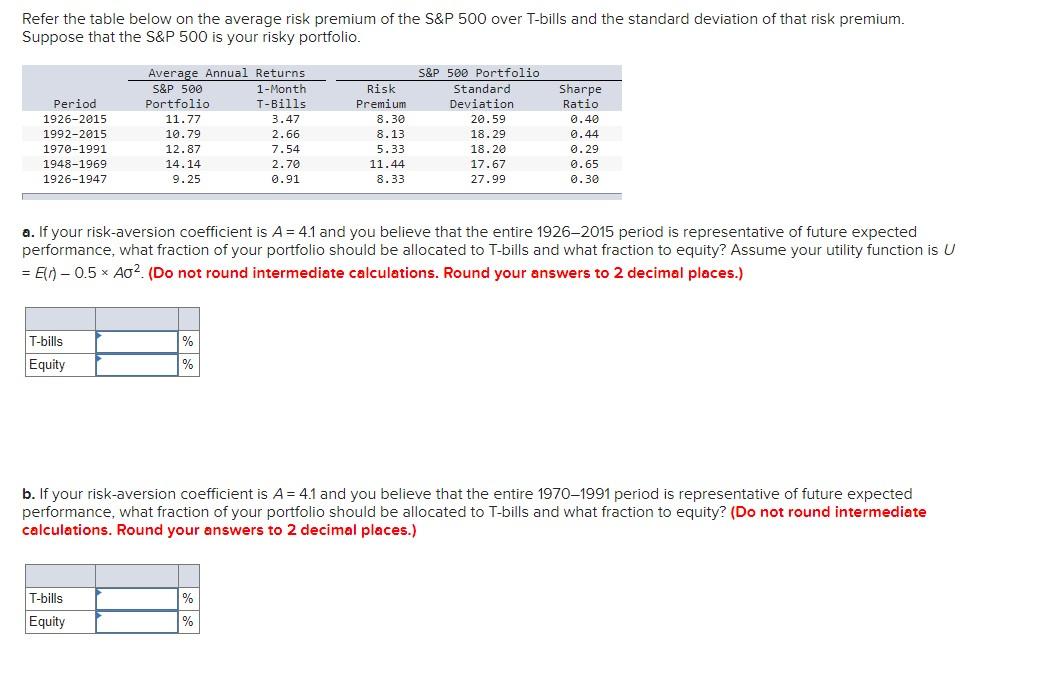

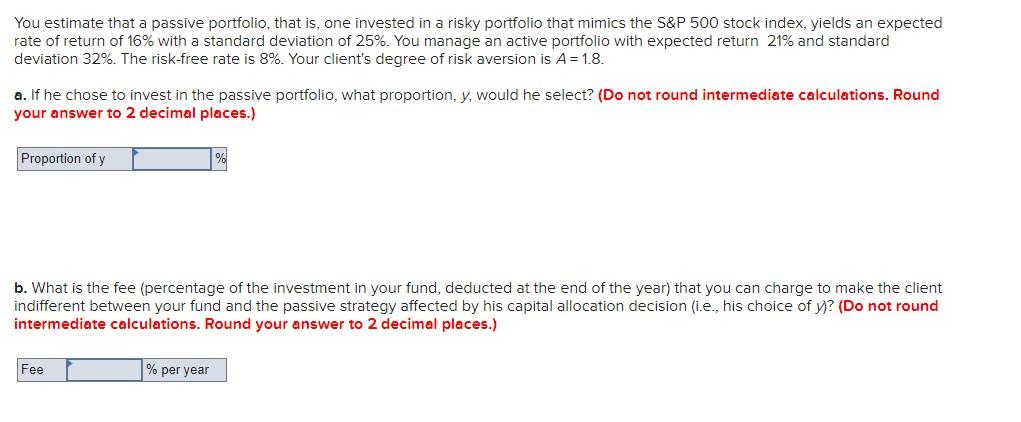

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio. Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1 - Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 Risk Premium 8.30 8.13 5.33 11.44 8.33 S&P 500 Portfolio Standard Deviation 20.59 18.29 18.20 17.67 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30 a. If your risk-aversion coefficient is A = 4.1 and you believe that the entire 1926-2015 period is representative of future expected performance, what fraction of your portfolio should be allocated to T-bills and what fraction to equity? Assume your utility function is U = E(1) - 0.5 ~ A02. (Do not round intermediate calculations. Round your answers to 2 decimal places.) % T-bills Equity % b. If your risk-aversion coefficient is A = 4.1 and you believe that the entire 19701991 period is representative of future expected performance, what fraction of your portfolio should be allocated to T-bills and what fraction to equity? (Do not round intermediate calculations. Round your answers to 2 decimal places.) % T-bills Equity % You estimate that a passive portfolio, that is, one invested in a risky portfolio that mimics the S&P 500 stock index, yields an expected rate of return of 16% with a standard deviation of 25%. You manage an active portfolio with expected return 21% and standard deviation 32%. The risk-free rate is 8%. Your client's degree of risk aversion is A=1.8. a. If he chose to invest in the passive portfolio, what proportion, y, would he select? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Proportion of y b. What is the fee (percentage of the investment in your fund, deducted at the end of the year) that you can charge to make the client indifferent between your fund and the passive strategy affected by his capital allocation decision (i.e., his choice of y)? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Fee % per year

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts