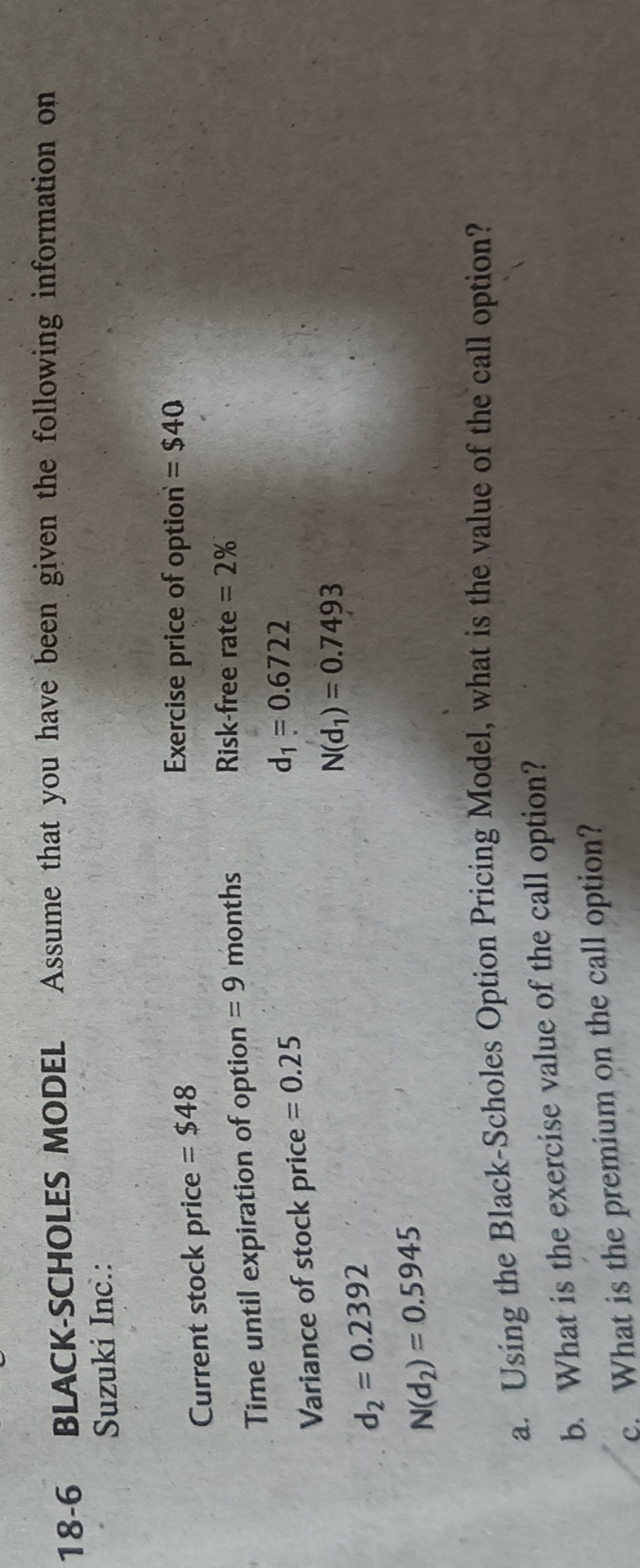

Question: 1 8 - 6 BLACK - SCHOLES MODEL Assume that you have been given the following information on Suzuki Inc.: Current stock price = $

BLACKSCHOLES MODEL Assume that you have been given the following information on Suzuki Inc.:

Current stock price $

Time until expiration of option months

Variance of stock price

Exercise price of option $

Riskfree rate

a Using the BlackScholes Option Pricing Model, what is the value of the call option?

b What is the exercise value of the call option?

c What is the premium on the call option?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock