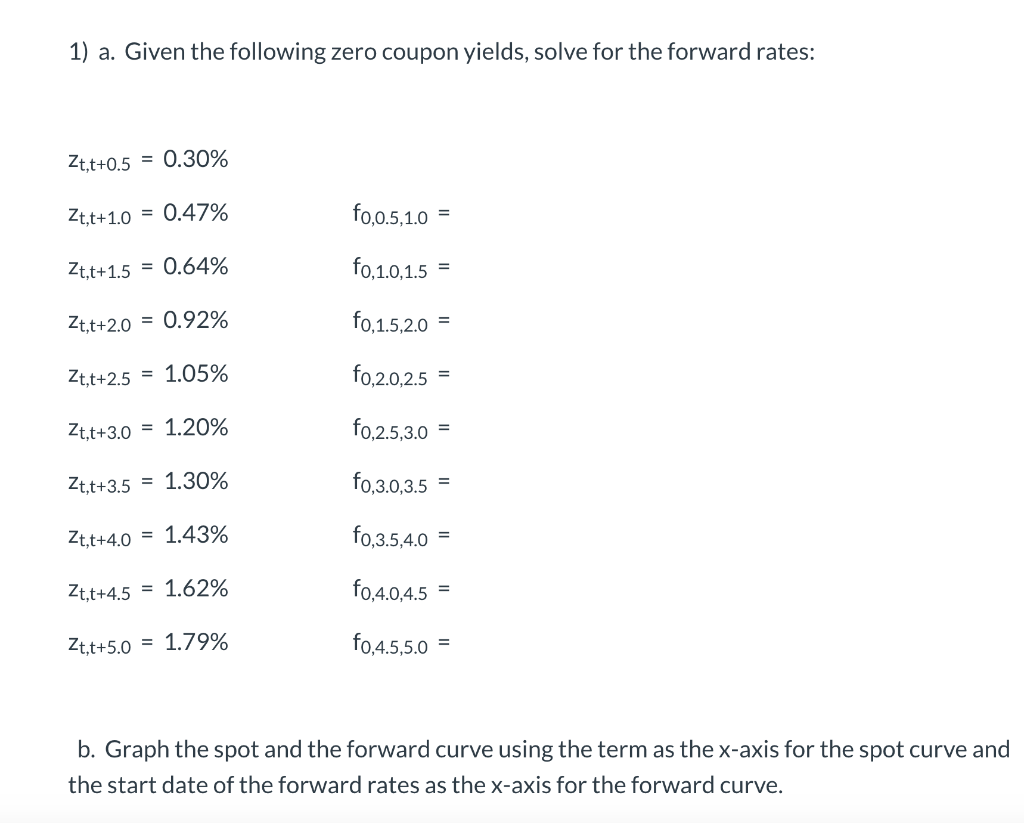

Question: 1) a. Given the following zero coupon yields, solve for the forward rates: Zt,t+0.5 = 0.30% Zt;t+1.0 = 0.47% f0,0.5,1.0 = Zt,t+1.5 = 0.64% f0,1.0.1.5

1) a. Given the following zero coupon yields, solve for the forward rates: Zt,t+0.5 = 0.30% Zt;t+1.0 = 0.47% f0,0.5,1.0 = Zt,t+1.5 = 0.64% f0,1.0.1.5 = Zt,t+2.0 = 0.92% f0,1.5,2.0 = Zt;t+2.5 = 1.05% fo.2.0.2.5 = Zt,t+3.0 = 1.20% f0,2.5,3.0 = Zt,t+3.5 = 1.30% f0,3.0,3.5 = Zt,t+4.0 = 1.43% f0,3.5,4.0 = Zt,t+4.5 = 1.62% f0,4.0,4.5 = Zt.t+5.0 = 1.79% f0,4.5,5.0 = b. Graph the spot and the forward curve using the term as the x-axis for the spot curve and the start date of the forward rates as the x-axis for the forward curve

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock