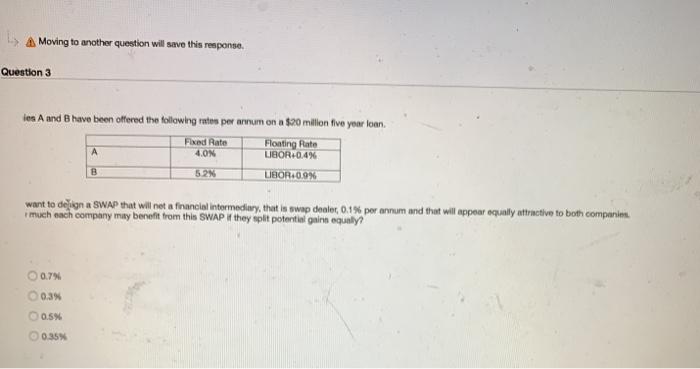

Question: 1 A Moving to another question will save this response. Question 3 les A and B have been offered the following rates per annum on

1 A Moving to another question will save this response. Question 3 les A and B have been offered the following rates per annum on a $20 million five year loan Fixed Rate Floating Rate 4.ON UBOR 0.4% B 52N UBOR.0.9% want to deign a SWAP that will not a francial intermediwy, that is swap dealer, 0.1% per annum and that will appear equally attractive to both companim. much each company many benefit from this SWAP If they plt potential gains equally 0.7% 0.3% 0.5% 0.35%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock