Question: 1. Basic concepts Finance, or financial management, requires the knowledge and precise use of the language of the field. Match the terms relating to the

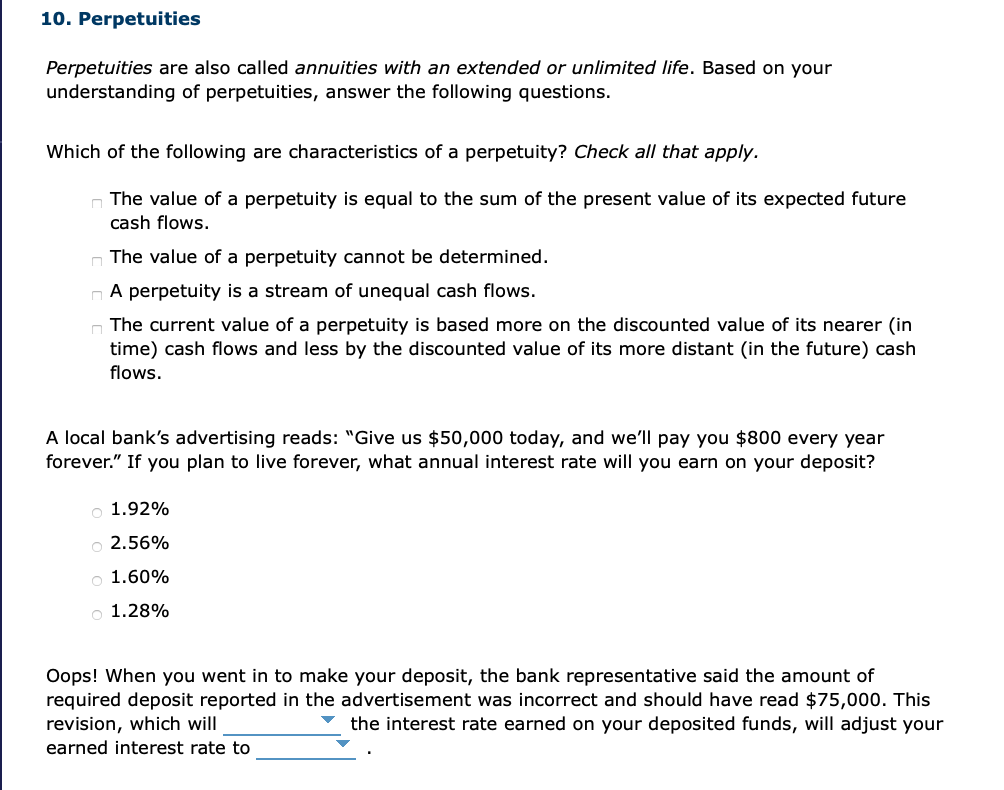

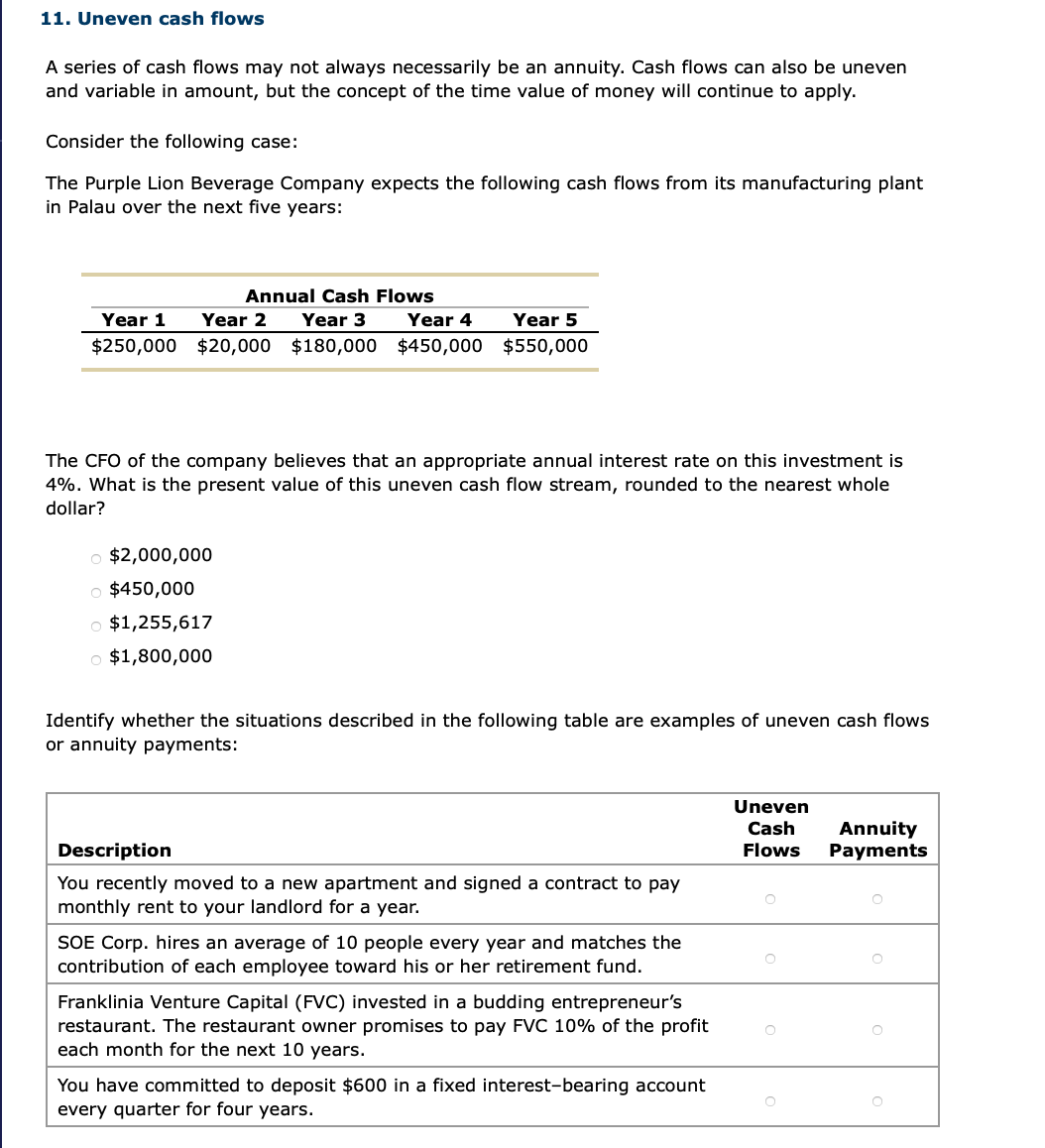

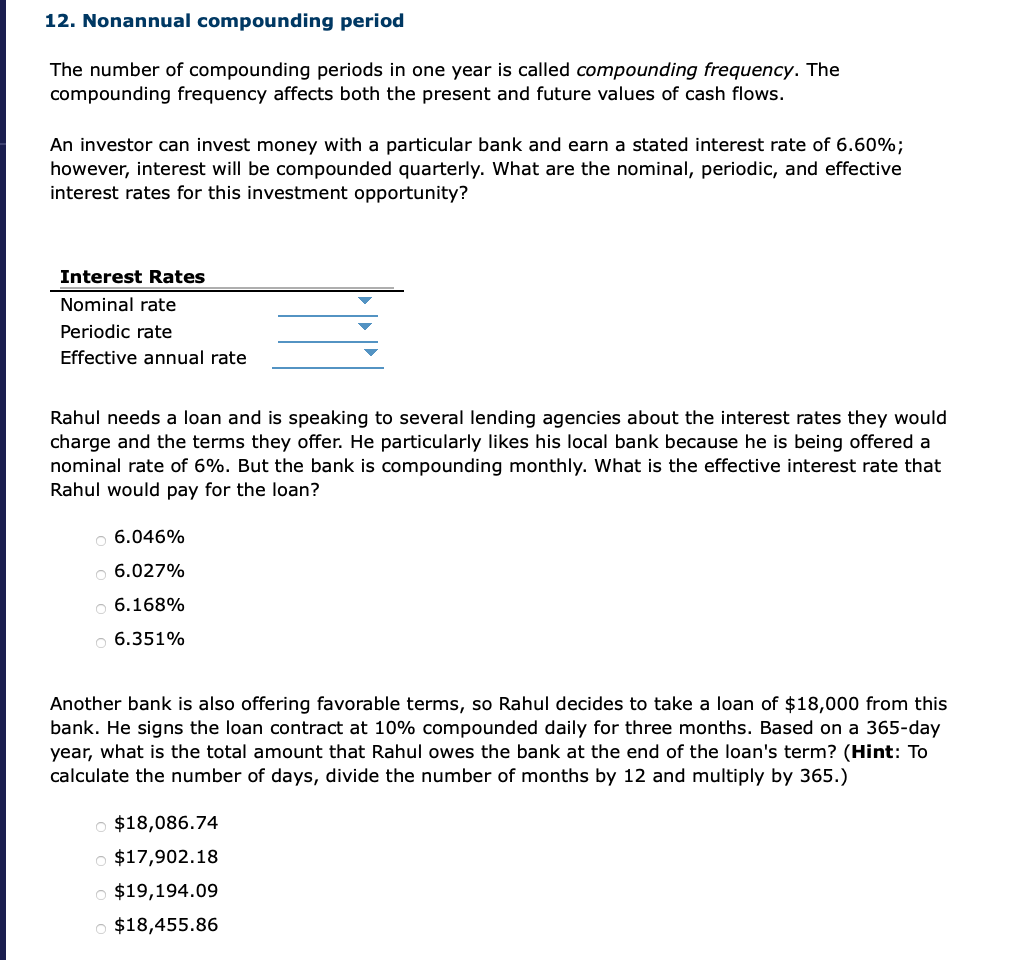

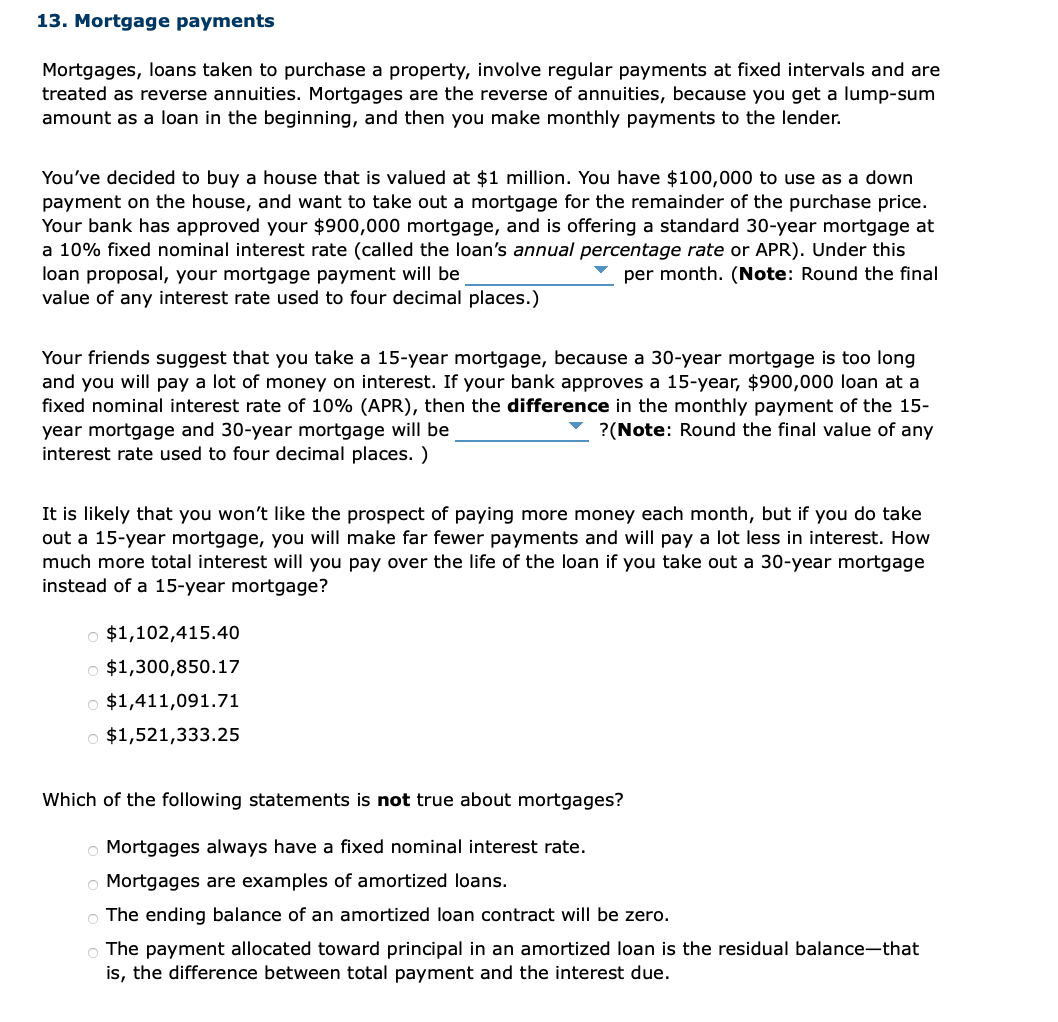

1. Basic concepts Finance, or financial management, requires the knowledge and precise use of the language of the field. Match the terms relating to the basic terminology and concepts of the time value of money on the left with the descriptions of the terms on the right. Read each description carefully and type the letter of the description in the Answer column next to the correct term. These are not necessarily complete definitions, but there is only one possible answer for each term. Term Discounting Time value of money Amortized loan Ordinary annuity Annual percentage rate Annuity due Perpetuity Future value Amortization schedule Opportunity cost of funds Answer Description The process of determining the present value of a cash flow or series of cash flows to be received or paid in the future. A cash flow stream that is generated by a share of preferred stock that is expected to pay dividends every quarter indefinitely. A series of equal cash flows that occur at the end of each of the equally spaced intervals (such as daily, monthly, quarterly, and so on). A concept that maintains that the owner of a cash flow will value it differently, depending on when it occurs. A table that reports the results of the disaggregation of each payment on an amortized loan, such as a mortgage, into its interest and loan repayment components. One of the four major time value of money terms; the amount to which an individual cash flow or series of cash payments or receipts will grow over a period of time when earning interest at a given rate of interest. A type of security that is frequently used in mortgages and requires that the loan payment contain both interest and loan principal. A cash flow stream that is created by a lease that requires the payment to be paid on the first of each month and a lease period of three years. A 6% return that you could have earned if you had made a particular investment. A value that represents the interest paid by borrowers or earned by lenders, expressed as a percentage of the amount borrowed or invested over a 12-month period. Time value of money calculations can be solved using a mathematical equation, a financial calculator, or a spreadsheet. Which of the following equations can be used to solve for the future value of an annuity due? PMT x {[(1 + N2 - 1]/r} FV/(1 + r)n PMT x {[(1 + N - 1]/r} x (1 +71) PMT x ({1 -[1/(1 + )]}/ x (1 +7r) 7. Future value of annuities There are two categories of cash flows: single cash flows, referred to as \"lump sums,\" and annuities. Based on your understanding of annuities, answer the following questions. Which of the following statements about annuities are true? Check all that apply. An annuity is a series of equal payments made at fixed intervals for a specified number of periods. An annuity due is an annuity that makes a payment at the beginning of each period for a certain time period. An annuity due earns more interest than an ordinary annuity of equal time. Ordinary annuities make fixed payments at the beginning of each period for a certain time period. Which of the following is an example of an annuity? A job contract that pays a regular monthly salary for three years A job contract that pays an hourly wage based on the work done on a particular day Luana loves shopping for clothes, but considering the state of the economy, she has decided to start saving. At the end of each year, she will deposit $570 in her local bank, which pays her 6% annual interest. Luana decides that she will continue to do this for the next four years. Luana's savings are an example of an annuity. How much will she save by the end of four years? $1,975.11 $2,643.14 $2,493.53 $2,119.50 If Luana deposits the money at the beginning of every year and everything else remains the same, she will save by the end of four years. 8. Present value of annuities and annuity payments The present value of an annuity is the sum of the discounted value of all future cash flows. You have the opportunity to invest in several annuities. Which of the following 10-year annuities has the greatest present value (PV)? Assume that all annuities earn the same positive interest rate. An annuity that pays $500 at the beginning of every six months An annuity that pays $500 at the end of every six months An annuity that pays $1,000 at the beginning of each year An annuity that pays $1,000 at the end of each year An ordinary annuity selling at $3,806.77 today promises to make equal payments at the end of each year for the next six years (N). If the annuity's appropriate interest rate (I) remains at 5.00% during this time, the annual annuity payment (PMT) will be Vo, You just won the lottery. Congratulations! The jackpot is $10,000,000, paid in six equal annual payments. The first payment on the lottery jackpot will be made today. In present value terms, you really won assuming annual interest rate of 5.00%. 9. Implied interest rate and period Consider the case of the following annuities, and the need to compute either their expected rate of return or duration. Matthew needed money for some unexpected expenses, so he borrowed $3,900.55 from a friend and agreed to repay the loan in four equal installments of $1,100 at the end of each year. The agreement is offering an implied interest rate of v Matthew's friend, Gregory, has hired a financial planner for advice on retirement. Considering Gregory's current expenses and expected future lifestyle changes, the financial planner has stated that once Gregory crosses a threshold of $4,136,860 in savings, he will have enough money for retirement. Gregory has nothing saved for his retirement yet, so he plans to start depositing $40,000 in a retirement fund at a fixed rate of 5.00% at the end of each year. It will take for Gregory to reach his retirement goal. 10. Perpetuities Perpetuities are also called annuities with an extended or unlimited life. Based on your understanding of perpetuities, answer the following questions. Which of the following are characteristics of a perpetuity? Check all that apply. The value of a perpetuity is equal to the sum of the present value of its expected future cash flows. The value of a perpetuity cannot be determined. A perpetuity is a stream of unequal cash flows. The current value of a perpetuity is based more on the discounted value of its nearer (in time) cash flows and less by the discounted value of its more distant (in the future) cash flows. A local bank's advertising reads: \"Give us $50,000 today, and we''ll pay you $800 every year forever.\" If you plan to live forever, what annual interest rate will you earn on your deposit? 1.92% 2.56% 1.60% 1.28% Oops! When you went in to make your deposit, the bank representative said the amount of required deposit reported in the advertisement was incorrect and should have read $75,000. This revision, which will the interest rate earned on your deposited funds, will adjust your earned interest rate to v 11. Uneven cash flows A series of cash flows may not always necessarily be an annuity. Cash flows can also be uneven and variable in amount, but the concept of the time value of money will continue to apply. Consider the following case: The Purple Lion Beverage Company expects the following cash flows from its manufacturing plant in Palau over the next five years: Annual Cash Flows Year 1 Year 2 Year 3 Year 4 Year s $250,000 $20,000 $180,000 $450,000 $550,000 The CFO of the company believes that an appropriate annual interest rate on this investment is 4%. What is the present value of this uneven cash flow stream, rounded to the nearest whole dollar? $2,000,000 $450,000 $1,255,617 $1,800,000 Identify whether the situations described in the following table are examples of uneven cash flows or annuity payments: Uneven Cash Annuity Description Flows Payments You recently moved to a new apartment and signed a contract to pay monthly rent to your landlord for a year. SOE Corp. hires an average of 10 people every year and matches the contribution of each employee toward his or her retirement fund. Franklinia Venture Capital (FVC) invested in a budding entrepreneur's restaurant. The restaurant owner promises to pay FVC 10% of the profit each month for the next 10 years. You have committed to deposit $600 in a fixed interest-bearing account every quarter for four years. 12. Nonannual compounding period The number of compounding periods in one year is called compounding frequency. The compounding frequency affects both the present and future values of cash flows. An investor can invest money with a particular bank and earn a stated interest rate of 6.60%; however, interest will be compounded quarterly. What are the nominal, periodic, and effective interest rates for this investment opportunity? Interest Rates Nominal rate v Periodic rate v Effective annual rate v Rahul needs a loan and is speaking to several lending agencies about the interest rates they would charge and the terms they offer. He particularly likes his local bank because he is being offered a nominal rate of 6%. But the bank is compounding monthly. What is the effective interest rate that Rahul would pay for the loan? 6.046% 6.027% 6.168% 6.351% Another bank is also offering favorable terms, so Rahul decides to take a loan of $18,000 from this bank. He signs the loan contract at 10% compounded daily for three months. Based on a 365-day year, what is the total amount that Rahul owes the bank at the end of the loan's term? (Hint: To calculate the number of days, divide the number of months by 12 and multiply by 365.) $18,086.74 $17,902.18 $19,194.09 $18,455.86 13. Mortgage payments Mortgages, loans taken to purchase a property, involve regular payments at fixed intervals and are treated as reverse annuities. Mortgages are the reverse of annuities, because you get a lump-sum amount as a loan in the beginning, and then you make monthly payments to the lender. You've decided to buy a house that is valued at $1 million. You have $100,000 to use as a down payment on the house, and want to take out a mortgage for the remainder of the purchase price. Your bank has approved your $900,000 mortgage, and is offering a standard 30-year mortgage at a 10% fixed nominal interest rate (called the loan's annual percentage rate or APR). Under this loan proposal, your mortgage payment will be per month. (Note: Round the final value of any interest rate used to four decimal places.) Your friends suggest that you take a 15-year mortgage, because a 30-year mortgage is too long and you will pay a lot of money on interest. If your bank approves a 15-year, $900,000 loan at a fixed nominal interest rate of 10% (APR), then the difference in the monthly payment of the 15- year mortgage and 30-year mortgage will be ?(Note: Round the final value of any interest rate used to four decimal places. ) It is likely that you won't like the prospect of paying more money each month, but if you do take out a 15-year mortgage, you will make far fewer payments and will pay a lot less in interest. How much more total interest will you pay over the life of the loan if you take out a 30-year mortgage instead of a 15-year mortgage? $1,102,415.40 $1,300,850.17 $1,411,091.71 $1,521,333.25 Which of the following statements is not true about mortgages? Mortgages always have a fixed nominal interest rate. Mortgages are examples of amortized loans. The ending balance of an amortized loan contract will be zero. The payment allocated toward principal in an amortized loan is the residual balancethat is, the difference between total payment and the interest due. 14. Loan amortization and capital recovery Ian loaned his friend $20,000 to start a new business. He considers this loan to be an investment, and therefore requires his friend to pay him an interest rate of 7% on the loan. He also expects his friend to pay back the loan over the next four years by making annual payments at the end of each year. Ian texted and asked that you help him calculate the annual payments that he should expect to receive so that he can recover his initial investment and earn the agreed-upon 7% on his investment. Calculate the annual payment and complete the following capital recovery schedule: Beginning Year Amount Payment Interest Paid Principal Paid Ending Bala 1 $20,000.00 v v v 2 w w - w 3 w w - - 4 w w - - - - Y 15. More on the time value of money Lloyd is a divorce attorney who practices law in Florida. He wants to join the American Divorce Lawyers Association (ADLA), a professional organization for divorce attorneys. The membership dues for the ADLA are $550 per year and must be paid at the beginning of each year. For instance, membership dues for the first year are paid today, and dues for the second year are payable one year from today. However, the ADLA also has an option for members to buy a lifetime membership today for $5,000 and never have to pay annual membership dues. Obviously, the lifetime membership isn't a good deal if you only remain a member for a couple of years, but if you remain a member for 40 years, it's a great deal. Suppose that the appropriate annual interest rate is 7.5%. What is the minimum number of years that Lloyd must remain a member of the ADLA so that the lifetime membership is cheaper (on a present value basis) than paying $550 in annual membership dues? (Note: Round your answer up to the nearest year.) 21 years 12 years 16 years 14 years In 1626, Dutchman Peter Minuit purchased Manhattan Island from a local Native American tribe. Historians estimate that the price he paid for the island was about $24 worth of goods, including beads, trinkets, cloth, kettles, and axe heads. Many people find it laughable that Manhattan Island would be sold for $24, but you need to consider the future value (FV) of that price in more current times. If the $24 purchase price could have been invested at a 5.75% annual interest rate, what is its value as of 2018 (392 years later)? $67,226,047,478.59 $90,952,887,765.15 $79,089,467,621.87 $104,398,097,260.87 Nick Nohitter's Contract Evaluation Worksheet Assumptions and 10 11 12 13 14 15 16 17 18 19 A Calculated Values Bank Rate Information: Nick's Bank Account Rate (compounded monthly) Monthly Bank Rate Effective Annual Interest Rate Salary and Bonus Information: Annual Salary (4% COLA) Monthly Salary Discount factor (based on Cell B4 above) Discounted Annual Salary Time-in-League Bonus Discount factor (based on Cell B4 above) Discounted Time-in- League Bonus Milestone Bonus Discount factor (based on Cell B5 above) Discounted Milestone Bonus B c % % % Year 1 Year 2 11.681222004 11.11267639 0.9754 0.9513 0.9050 Year 3 10.571802890 0.8610 Year 4 10.057254654195 0.8191 Total value 19 20 21 22 23 24 25 26 27 28 29 30 Discounted Milestone Bonus Performance Bonus Discount factor (based on Cell B5 above) Discounted Performance Bonus Monthly Endorsement Contract Payment Discount factor (based on Cell B4 above) Discounted Monthly Endorsement Payment Contract's Total Nominal Value Contract's Total Discounted Value 0.9513 0.9050 0.8610 0.8191 11.6812 11.1127 1. Given your worksheet calculations, which of the following statements is accurate? Is Michael's estimate of the value of Nick's contract accurate on either a nominal or discounted basis? Check all that apply. It is appropriate and necessary to discount the performance bonus using the bank account's effective annual interest rate because of differences in the timing of the compounding of the bank account and that of the payments for the performance bonus. It is appropriate and necessary to discount the endorsement contract using the bank account's effective annual interest rate because of differences in the timing of the compounding of the bank account and that of the payments on the endorsement contract. Michael's estimate of the nominal value of Nick's contract is correct. Related Question: The local car dealer creating Nick's endorsement opportunity can earn 6% (compounded quarterly) on his deposited funds. She would have to deposit each quarter, starting exactly two years before the day Nick signs his contract, to fund her endorsement contract. [Note: The future value interest factor of 6% compounded quarterly for eight quarterly periods is 8.4328.]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!